The Future of Gold: A Very Long-Term Uptrend

(June 7, 2016 - by Seeking Alpha)

Summary

Strong first quarter in 2016 with price appreciation of approximately 25% demarcated beginning of new long term uptrend.

Long term uptrend in price to be driven by gold’s role as secure haven amidst global economic uncertainty.

Central banks and investment banks purchasing large quantities of gold bullion.

Leading hedge funds endorse gold as core investment while exiting stocks.

"I did not know that mankind were suffering for want of gold. I have seen a little of it. I know that it is very malleable, but not so malleable as wit. A grain of gold will gild a great surface, but not so much as a grain of wisdom."

? Henry David Thoreau, Life Without Principle

In the midst of strengthening opinion that it will rise in importance as an international currency, gold jumped in price by approximately 25% in the first quarter of 2016. In addition to commodity market factors underlying this strong breakout, global economies bear all the hallmarks of being in transition to an uncertain future. In such a crucible gold may enjoy the added impetus of becoming an economic safe haven amidst the turbulence of international markets.

This article discusses the forward long term direction of gold. Recent short term considerations such as the FOMC minutes have provided a passing downward nudge to price. This is the most recent of what will no doubt be many acts in a play extending over many years to come. It is frequently the case with emergent uptrends that after initially breaking through resistance a retracement occurs before resumption of the new upward direction. That fact speaks to the importance of timing an entry. The eventual long term direction of gold is the question examined here.

New Long Term Upward Trend

A daily gold price chart shows the significant market upturn that commenced at the beginning of January 2016.

Gold Price in US Dollars data by YCharts

After a markedly positive first quarter the question becomes: is this the beginning of a long term uptrend or a mere retracement in a continuing down trend? The following weekly chart addresses this debate from a technical standpoint. The raison d’etre of the TrendSpotter indicator shown is to identify nascent trends.

Demarcation of a new uptrend commencing at the beginning of 2016 at a healthy angle of 45 degrees is clearly shown by TrendSpotter and confirmed by the Relative Strength Index rising above a reading of 50, the fault line that distinguishes uptrends from downtrends. While the market may initially prevaricate around this fault line, the likelihood is that the continued direction will be upward. RSI 21 has also exhibited an extended positive divergence since mid 2013, reinforcing the case for the emergence of a long term uptrend.

Investment banks are purchasing large amounts of gold bullion for their own accounts (see Seeking Alpha "Goldman Sachs: Reputation And Credibility Are Buzzed"), quantifying their belief in the order of magnitude of its coming price appreciation. Strengthening this view gold for the first time has a positive carry in many parts of the world as bankers experiment with negative interest rates. JP Morgan Chase & Co. (NYSE:JPM) is recommending that its clients position for a new and very long bull market in gold.

Prominent Hedge Funds Go To Gold

Leading hedge funds the Duquesne Family Office, Green Light Capital and Elliott Management have publicly taken a stand in the gold camp. Stanley Druckenmiller, chair and CEO of the Duquesne Family Office, in an address to the Sohn Investment Conference on May 4, 2016 stated that the economy is in the longest ever period of excessively easy monetary policies. He maintains that while ending quantitative easing, the Fed’s radical dovishness persists. Druckenmiller recommends that investors withdraw from stock markets, which he believes are becoming exhausted, and asserts that his core investment and greatest currency allocation is gold.

David Einhorn of Greenlight Capital Inc. is also bullish on gold as he sees the world’s central bankers continuing to ease monetary policy. Einhorn criticized the European Central Bank’s low borrowing costs, increased asset purchases and borrowing subsidies, which have implicitly devalued the euro. He holds that the imposition by the Bank of Japan of a negative interest rate policy and the lowered forecasts for U.S. rate hikes will also likely contribute to significantly raising the value of gold.

Paul Singer of Elliott Management believes that investors are understanding that the world’s central bankers are effectively debasing their respective currencies. He contends that as confidence in the judgment of central bankers wanes, the positive effect on gold price will be powerful.

Central Banks Are Strong Buyers Of Gold

These leading hedge fund opinions have been arrived at in the context of the figurative printing of money by central banks, their buying of gold, reduced production at gold mines, and the economic difficulties being experienced by the European Union and China.

In tacit recognition of the flip side of their easing policies central banks have since 2010 been net buyers of gold, and their demand has expanded rapidly. They added 477.2 metric tonnes to their reserves in 2014, the second-biggest increase in 50 years and 17 percent more than the previous year, according to the World Gold Council. The strongest year of central bank gold purchases in nearly 50 years was 2012, well into the era of quantitative easing, as central bankers attempted to bulwark against the inevitable inflationary consequences of their policies. In 2016 central banks have remained strong buyers, purchasing 109 metric tonnes in the first quarter.

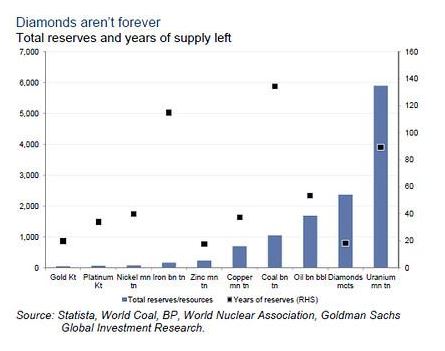

The following chart of reserves of natural resources and years of supply remaining shows that there are only 20 years of identified minable gold resources left worldwide, a consideration that will surely drive strong appreciation in the price of gold given it’s economic role, industrial applications for which there are no substitutes, and consumer demand.

The reflexive web that connects stock market performance, interest rates, value of the dollar, national debt and the price of gold, when evaluated as to the direction of its individual components strongly indicates a protracted rise in the price of gold.

Economic Elements Drive Rising Gold

The underlying price structure of the rise in the stock market since 2009 is weak, displaying negative divergence as shown in the monthly chart of the Dow Jones Composite, and may be on the cusp of entering a down cycle.

Source: Dow Jones

The expectation of higher interest rates is questioned and uncertain, not least because the Fed has shown despite its statements to the contrary that it pays great deference to the stock market when making rate decisions. The S&P 500 has not made a new high since May 2015.

^SPX data by YCharts

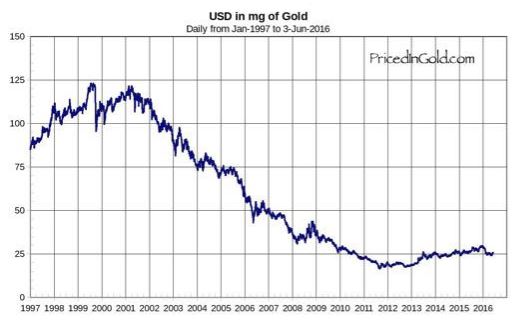

The dollar has not achieved a new high against the pound since December 2008, and has been falling markedly against the yen since May 2015. The value of the dollar in gold, charted below, has decayed from approximately 120 mg of gold in 2001 to only approximately 25 mg in early June 2016

Source: PricedinGold.com

Vulnerability Of U.S. To Action By Creditors

There are concerns about the vulnerability of the U.S. economy to the changing circumstances and future actions of two of its major creditors, Saudi Arabia and China. Saudi Arabia has indicated that it may sell as much as $750 billion in treasuries and other U.S. debt if U.S. law is changed to make Saudi Arabia potentially liable for the 9/11 terrorist attacks. Sales of this size would undoubtedly lower the valuation of the U.S. dollar and U.S. debt. Saudi Arabia is suffering from its own economic problems stemming from the fall in the price of oil, making sale of its currency reserves in the form of U.S. treasuries all the more likely.

China effectively printed yuan and bought dollars for years to hold down its currency while enjoying a huge trade surplus. Since then China’s reduced GDP growth has led markets to take the yuan lower against the dollar. Recent concerns about the accounting of debt in the Chinese economy may exacerbate weakening of the yuan. In response the Peoples’ Bank of China is selling tranches of its foreign currency reserves, much of it in U.S. treasuries. That fact will exert strong downward influence on the price of U.S. debt and on the dollar with resultant constraints on the Fed’s ability to raise rates.

If these market processes weigh heavily on the dollar they may over a period of years threaten its role as the world’s reserve currency, potentially thrusting gold onto center stage as the metric for international valuation. The more unfolding events bring this eventuality into focus as even a possible outcome, the more the price of gold will strengthen.

Conclusion

The present short term retracement at resistance after the inception of a new long term uptrend represents an excellent opportunity to enter a long position in gold. The market offers reduced risk when near its cycle low, while the potential for very high yield from a long term position provides an outstanding projected asymmetric return.

Drivers of price appreciation will be gold’s role as the historically established commodity of secure value while world economies transition into doubt and uncertainty, speculation in a strongly rising market, industrial applications without substitute, and consumer demand.

-

Gold And Silver Trading Above Key Support Levels By

Gold And Silver Trading Above Key Support Levels ByApril 25 2024

-

-

Is Silver Going To Break Out On The Upside? By

Is Silver Going To Break Out On The Upside? ByApril 24 2024

-

Gold And Silver Trading Above Key Support Levels By

Gold And Silver Trading Above Key Support Levels ByApril 24 2024

-

Gold And Silver Test Key Support Levels And Hold By

Gold And Silver Test Key Support Levels And Hold ByApril 23 2024