Plunging dollar reveals market’s anxiety about Trumponomics

(June 8, 2017 - by Nicholas Spiro)

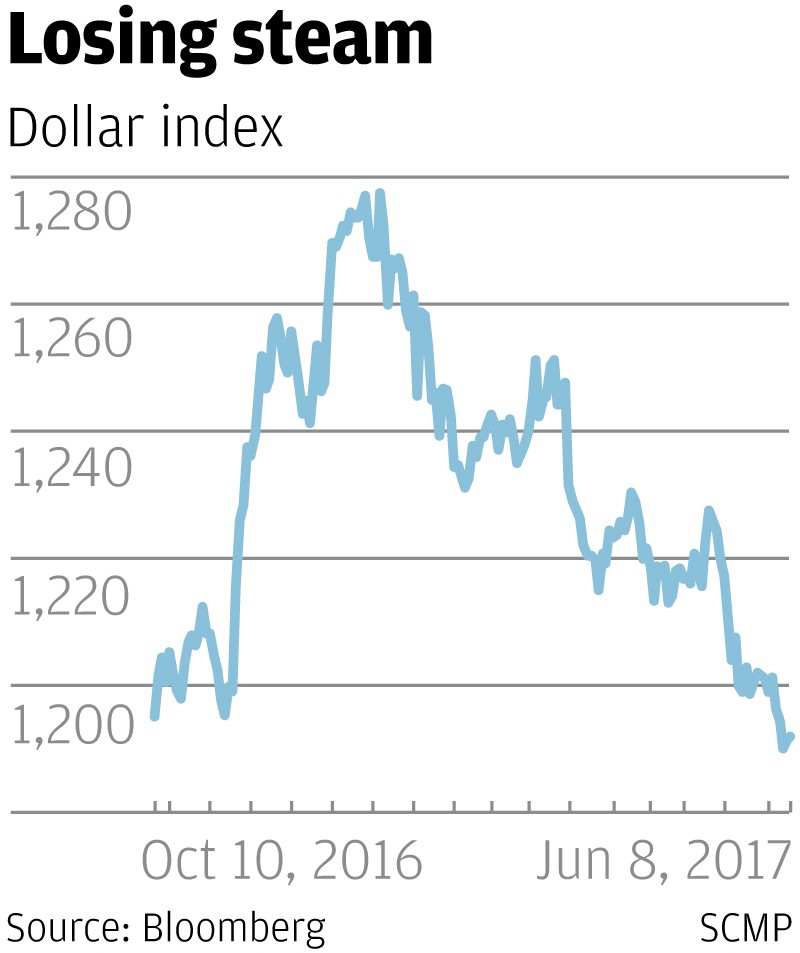

For the US dollar, the past seven months have been a tale of two halves.

Following the unexpected victory of Donald Trump in the US presidential election in November, the greenback surged as international investors positioned themselves for a period of faster growth and inflation based on expectations that Trump’s pro-business policies would easily pass through a Republican-dominated Congress.

Yet after hitting a 14-year high in early January, the dollar index, a gauge of the greenback’s performance against a basket of other currencies, began to fall sharply, mainly because of mounting concerns about Trump’s ability to push through his pro-growth agenda, but also, more recently, because of weaker-than-expected economic data.

{kind=link}

On Tuesday, the index fell to its lowest level since early October as investors questioned the scope for a further tightening in US monetary policy. While the Federal Reserve is still expected to raise interest rates again at its policy meeting next week, the renewed decline in inflation and waning confidence in Trump’s presidency are weighing heavily on the dollar.

After shooting up 5.5 per cent in the eight weeks following Trump’s victory on November 8, the index has since fallen 6.5 per cent, with more than two-thirds of the decline occurring since early April when Trump’s political woes deepened.

The plunge in the greenback, moreover, reveals a lot about the current state of sentiment in financial markets, both in developed and developing economies.

Just as the dollar’s retreat reflects a loss of confidence in “Trumponomics”, its decline is helping shore up emerging-market assets at a time when there are growing concerns about the spillover effects of China’s efforts to rein in its unruly shadow banking sector.

The three most important causes and effects of the dollar’s decline are:

? Trump impeachment risk: The dollar is becoming something of a proxy for sentiment towards the Trump administration and its ability to gain congressional approval for its much-anticipated policies of tax cuts and infrastructure spending aimed at invigorating the US economy. Multiple probes into alleged links between Trump’s election campaign team and Russia, given added urgency by Trump’s much-criticised decision to fire James Comey, the former head of the Federal Bureau of Investigation, have sparked accusations that Trump has obstructed justice. The whiff of impeachment is in the air.

The strain on the dollar this week stemmed mainly from fears that Comey’s eagerly awaited testimony to Congress on Thursday will lead to further allegations against Trump, crippling his presidency, which is already mired in scandals. On Wednesday, James Clapper, the former US director of national intelligence, said the Watergate scandal in the 1970s that led to the impeachment of former president Richard Nixon “pales” in comparison to the “assault on [American] institutions” perpetrated by Russia and Trump.

Make no mistake, the dollar has become a political currency and could fall further if Comey drops a bombshell that severely undermines Trump.

? Emerging-market benefits: While the dollar’s fall is a sign of waning confidence in Trump’s policy agenda, it is helping buoy sentiment towards emerging markets at a sensitive time for the asset class.

One of the reasons why the spillover effects from China’s crackdown on leveraged investment have been relatively contained – while commodity markets have come under pressure since the clampdown intensified in April, emerging-market assets have proved resilient – is that the currencies and local bond markets of developing economies are benefiting from the weaker dollar.

According to JPMorgan Chase, investors have been buying emerging-market domestic debt, even in the riskiest markets such as Turkey and South Africa. Local-currency bonds in developing economies have returned more than 11 per cent since the start of 2017, underpinned by strong gains in emerging-market currencies against the dollar.

? Euro surges: The flip side of a weaker dollar is a stronger euro. The greenback’s slump is helping fuel a rally in Europe’s single currency, which has shot up nearly 6 per cent since mid-April. Hedge funds have turned positive on the euro for the first time since 2014 as a result of a confluence of robust growth, diminishing political risk and improved corporate earnings. If the European Central Bank, which meets on Thursday, hints that it will start scaling back, or “tapering”, its asset purchases, the euro could strengthen further.

Still, a bit of perspective is in order.

The dollar was ripe for a correction, having surged more than 20 per cent since mid-2014, mainly because of the divergence in global monetary policies.

Last month’s fund manager survey by Bank of America Merrill Lynch also showed that long dollar positions remained one of the most popular trades.

The greenback could fall further, but it would still be declining from a very high level.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-