The Gold Standard, the Golden Jubilee and the Role of Gold in an Investment Portfolio

(8/12/22 - Olegs Jemeljanovs, PhD, CFA)

It came as no surprise to me that in today’s information-saturated world the jubilee of one of the most important economic events of the last hundred years had passed almost unnoticed last year. Moreover, this was the jubilee in its original, biblical meaning when once in 50 years the sold and mortgaged lands were returned to their original owners, slaves and prisoners of war were freed, debts were forgiven, and the land rested from field work. (As you can see the Bible can serve as a good source of information for studying not only moral and ethical, but also financial and economic, and even scientific and technical issues). Only later did other significant anniversaries begin to be called jubilees, specifically reserving the status of the golden jubilee for the 50th anniversary. So, let’s revisit this particular golden jubilee now. It is better late than never, as they say.

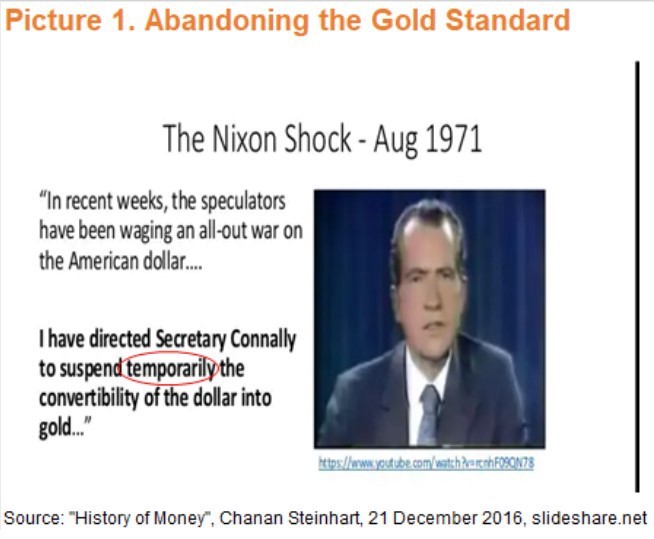

On 15 August 1971, US President Richard Nixon officially announced that the country was completely abandoning the gold standard. This meant that the US government abandoned the convertibility of US dollars into gold at a fixed rate of $35 per ounce. It is needless to say that the suspension of convertibility was presented as a “temporary” solution since there is nothing more permanent than something temporary (see Picture 1 below).

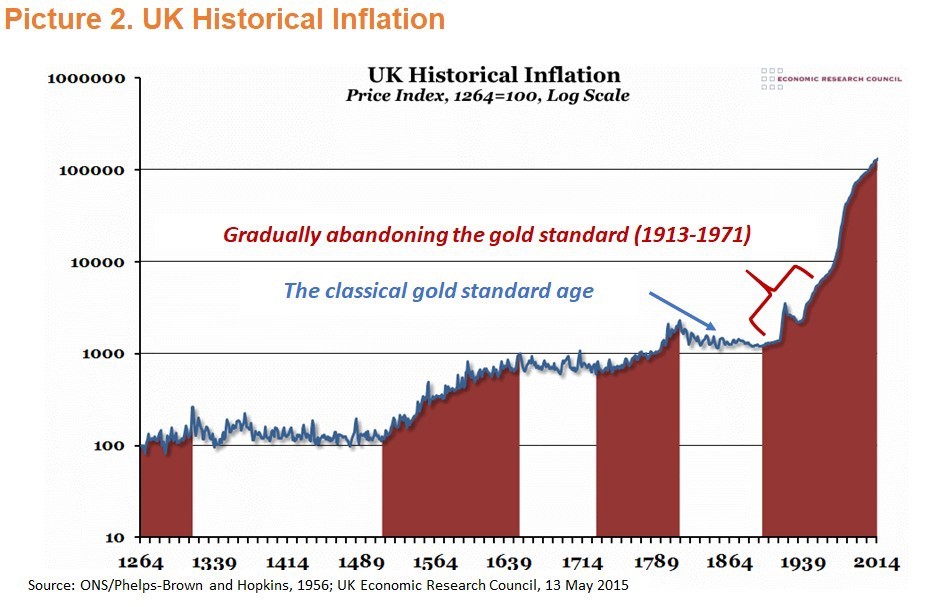

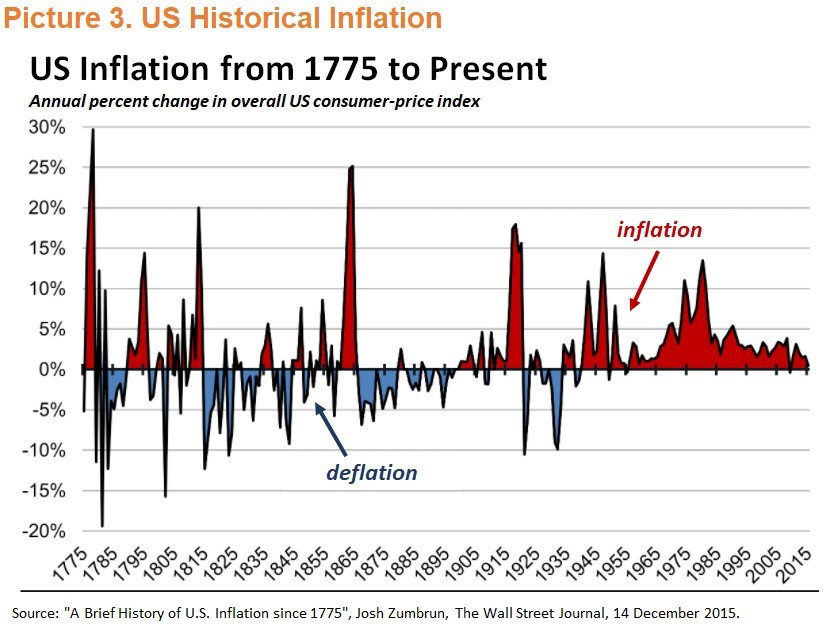

The financial system of most civilizations over the past three thousand years, in one form or another, was based on the silver, gold or bimetallic standard (gold and silver). Life under these standards was quite simple: if a country lived beyond its means, accumulating a large government budget and foreign trade deficit, and no one was willing to lend it gold and silver then it had to “tighten the belts”, reduce consumption and start thinking about how to live on. For example, it could try to invent some new technology or product, find a new export market or organize the production cycle more efficiently. In reality, of course, life was harsh and dynamic: during the 19th century and early in the 20th century the United Kingdom and the United States — the centers of the global financial system — experienced financial crises and panics every 8–10 years. But the gold standard system also had one advantage: stable prices (see Picture 2 below). Central banks simply did not have the ability to “adjust” the money supply, so periods of inflation alternated with periods of deflation (see Picture 3 below).

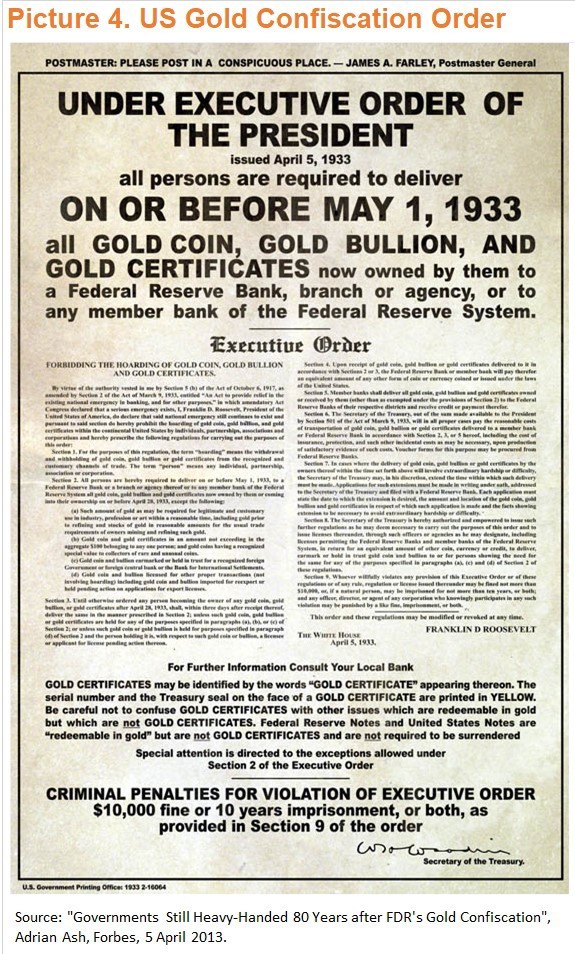

The dismantling of the gold standard system took place gradually. Early in the 20th century, following the dramatic financial panic of 1907, the US government decided to regulate the financial system more thoroughly by establishing the Federal Reserve System — the US central bank — in 1913. During the Great Depression, the US government even resorted to seizing gold (see Picture 4 below) from private citizens at the official price of $20.67 per ounce just to revalue it at a price of $35 per ounce a year later. Finally, in 1971 the US president was forced to finally abandon the US dollar’s peg to gold even for official settlements with the governments of other countries. The background of this decision was simple and understandable to any person who lived in the 19th century: due to various factors the United States had accumulated such a large foreign trade deficit with other countries that the US government simply could not meet the demand of the governments of these countries to exchange dollars received for goods and services for gold.

As a result, in the past 50 years we have been living in a new, experimental world of fiat money where the money supply is regulated to smooth the fluctuations of economic cycles. Perhaps the economic downturns have become milder due to the support of central banks but at the expense of higher consumer prices and asset values. It is interesting to note that the pace of scientific and technological progress began to decline in the early 1970s too. Maybe people have become over-reliant on central banks and less on their ability to get out of difficult situations on their own? It is probably too early to draw any definitive conclusions on this subject. But despite the fact that the famous economist John Maynard Keynes once called the gold standard system a “barbaric relic”, while the business partner of the equally famous investor Warren Buffett Charlie Munger believes that “…civilized people don’t buy gold”, gold’s appeal as an investment product, a safe asset and simply as a jewelry metal does not show any signs of decline. Why?

Gold has clearly benefitted from at least three thousand years of its use in the financial system. But taking a rational look at the situation, we must admit that there are many other objective factors that support gold’s continuing appeal.

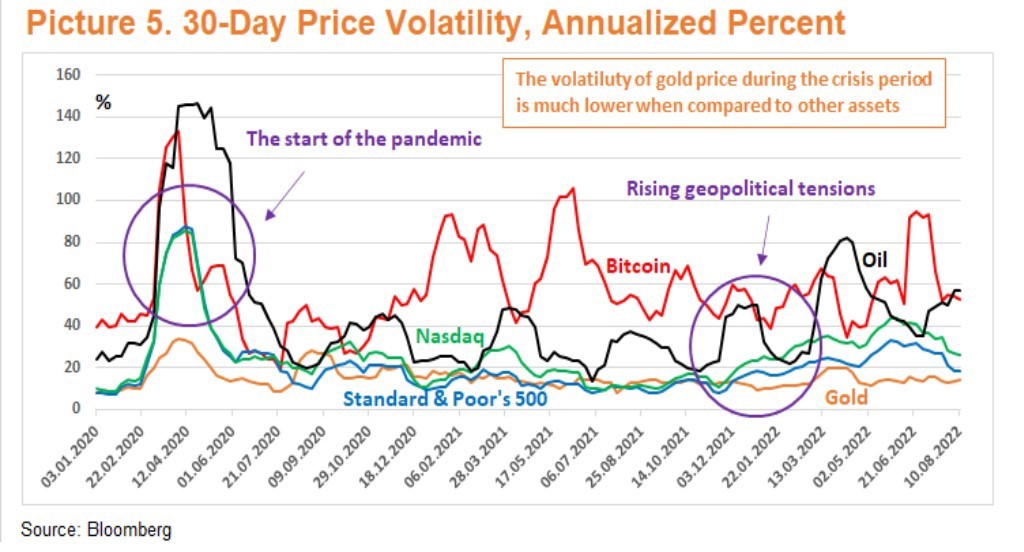

First, gold prices are much more stable compared to most other assets (see Picture 5 below), particularly during periods of crisis, which secures its status as a safe asset and a “stabilizer” of the investment portfolio.

Second, the demand for gold persists due to the fact that during periods of instability and higher price volatility, the price of gold tends to have a negative correlation with the prices of other assets (see Picture 6 below). This implies that in situations of financial stress gold prices often rise while prices for other assets fall, thereby increasing the role of gold as a universal “diversifier” of the investment portfolio, regardless of the source of financial stress. This differentiates gold from other ways to protect the value of your portfolio by using, for example, derivative financial instruments since these are focused on protecting the portfolio against some specific risks.

Third, a statistical analysis shows that there is an almost perfect correlation between the gold price, the US dollar exchange rate and real interest rates, which are affected by the level of inflation expectations, where the correlation coefficient reaches 0.94 (see Picture 7 below). For those who have forgotten / almost forgotten / did not know (select your option) mathematics, a correlation coefficient of 1 means that there is a perfect correlation. That is, the price of gold almost always climbs when the US dollar exchange rate declines, nominal (before taking inflation into account) interest rates fall and inflation expectations rise. At the same time, the price correlation of a new contender for the status of “digital gold” — bitcoin — with the US dollar exchange rate and real interest rates has been close to zero over the past three years. On the other hand, the price of bitcoin has had a consistently positive correlation with the Nasdaq technology stock index, thus implying that it is still trading similarly to other technological assets. This strengthens the traditional role of gold as a hedge against falling fiat money exchange rates and declining real interest rates.

That is why moderate investments in gold or a basket of precious metals (gold, silver, platinum, palladium) in the amount of 3 to 10% of your total portfolio can help stabilize it, diversify it as well as protect it from a fall in the value of your home currency or a decline in real yields on your interest-bearing investments.

Only investing in gold will not make you rich. Rather, this will be an insurance policy whose role will be to maintain your “vital minimum”.

As one Scottish proverb says, «Get what you can, and keep what you have, that’s the way to get rich”.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-