Will The Glitter Return To Gold Value In 2022?

(January 13th, 2022 - Tim Davies)

Gold should really be shining now. Inflation is emerging and with global economies still struggling to recover from COVID-19 related lockdowns, central banks will likely continue to stimulate with low interest rates and quantitative easing (‘printing money’). In this environment, hard assets that protect from monetary currency debasement should do well.

Yet gold and silver equities remain substantially below previous high-water marks that occurred in the previous inflation-led rallies of the 1970s, 2000s, and early 2010s. Many blame the ‘financialisation’ of gold – the massive increase in trading of futures and options contracts – for a low gold value.

But that could change in the new year with new global banking rules possibly igniting fresh interest from investors in an under-owned and long-forgotten asset class, particularly if inflation continues to accelerate. The changes should allow a return to fundamentals of gold value and let gold once again regain its role as a ‘monetary asset’ for investors.

Divorced from reality

Gold-related trading on global financial markets has become disconnected from supply and demand. When it comes to supply(1), the world’s gold reserves of 197,000 is today valued at US$11 Trillion (Global central bank holds approximately 20% of global gold reserves as reserve assets). Annual global mining for gold has plateaued at 3,200 tonnes per year since 2015. At today’s price of US$1,800/oz, this adds approximately US$180 billion per year of new supply to annual global gold reserves (+1.7% per year).

On the demand side, physical gold bullion demand for jewelry, and from industry and investors, has averaged approximately 4,200 tonnes or US$240 billion per year since 2010 (Figure 1)(2).

Figure 1: Annual global gold bullion demand (tonnes)

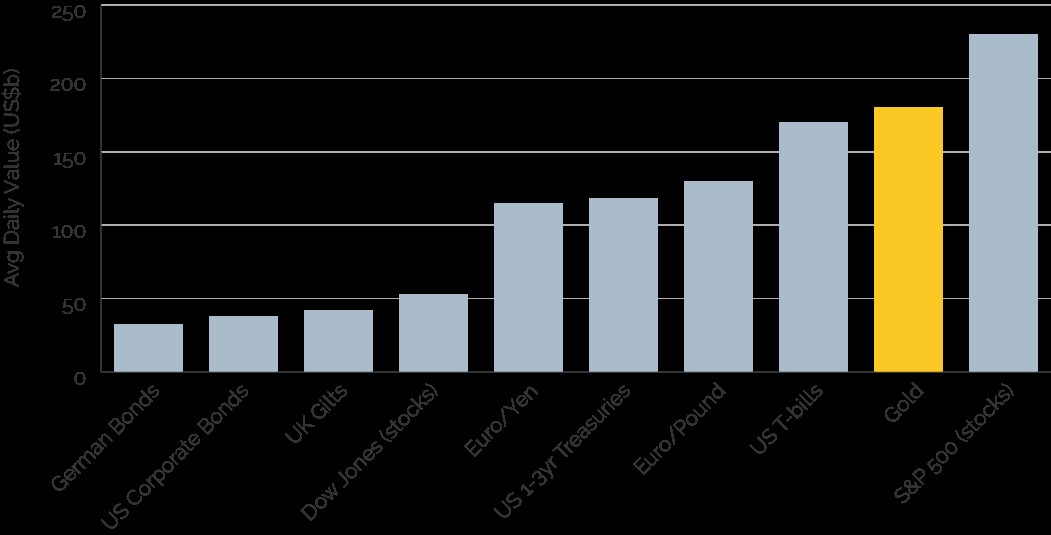

Trading volumes are 200 times greater than actual physical bullion demand, illustrating the extreme leverage and scale of trading in gold-related products. The total trading value of gold-related financial products has reached US$180 billion each day, the equivalent to 110% of the world’s entire annual gold mining output. Annual trading in gold-related financial products has now surpassed US$50 trillion, making it the second-most traded financial instrument in the world behind US S&P 500 equities trading (Figure 2).

Figure 2: Top 10 Financial Instruments by Avg Daily Trading value (US$b)

Suppressing prices

So, what has caused this ‘financialization’ of gold and a low gold value?

One of the challenges investing in physical bullion is the cost of metals delivery and vault storage. To get around this problem, and encourage much larger trading volumes, commodity futures exchange introduced ‘unallocated’ financial products. ‘Unallocated’ gold is where the gold remains the property of the bank and the investor is a creditor, as opposed to allocated gold which is owned outright by the investor.

Allocated gold allowed larger investors like banks and pension funds to place highly leveraged bets on the future price of precious metals without needing to hold the underlying physical metal.

With just 0.5% of the daily trading volume of gold products listed on financial exchanges, physical bullion quickly lost pricing discovery (basically the price set by supply and demand) to futures market pricing. That forced bullion miners and investors to accept the futures price for their physical bullion transactions.

Lax banking laws over the past few decades have also allowed global investment banks to build large, highly leveraged precious metals positions that in some cases were later found to have been used to manipulate financial market prices. Many investors believe precious metals have underperformed over the past few decades primarily because overleveraged financial products suppressed prices and led to a low gold value.

Lifting the veil

Following the 2008 global financial crisis, global banking regulators began to implement a series of banking laws (referred to as ‘Basel 3’) designed to strengthen the regulation, supervision and risk management of the banking industry.

From January 1, 2022, these changes are set to dramatically lower the use of leverage in precious metal related financial products (futures and options) including gold. Banks holding ‘unallocated’ gold and precious metal financial contracts must now allocate 70% more collateral for unallocated and leveraged bullion positions versus 2021 requirements.

The veil will finally be lifted on precious metal prices – and gold value — as bullion banks dramatically shrink unallocated positions on trading books.

Global bank regulatory shifts under Basel 3 rules will substantially reduce the ability of global central banks and bullion banks to suppress precious metals and control the ’low inflation environment’ narrative. In this context, investors might consider raising exposure to precious metals and related mining equities with gold value expected to rise as bullion banks are forced to retreat from their heavily leveraged precious metal positions.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-