China’s Gold Market Was Strong In March As Prices And Investment Increased While Imports And Jewelry Demand Fell

(April 15, 2025 - Ernest Hoffman, Kitco News)

(Kitco News) – China’s gold market showed significant strength in March and through Q1, with all-time highs in domestic prices and ETF inflows and ongoing central bank buying, but the yellow metal’s rally continues to sap imports and jewelry demand, according to Ray Jia, Research Head, China at the World Gold Council (WGC).

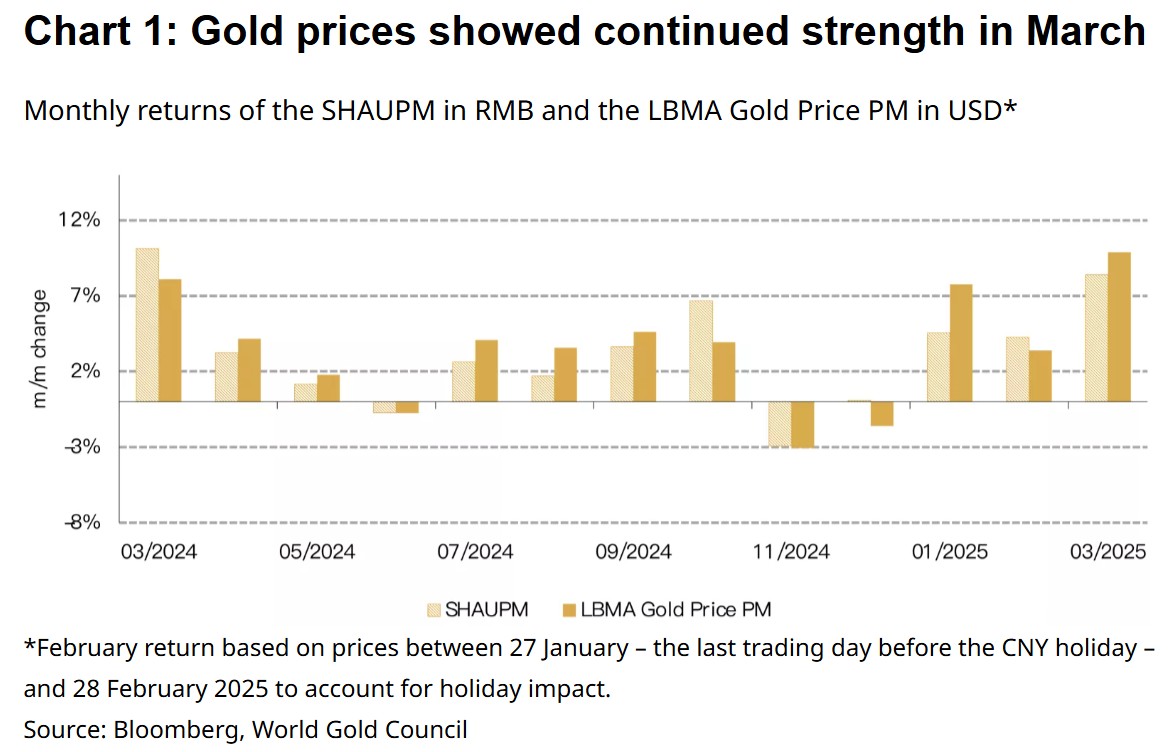

Jia noted that gold’s price rally continued unabated in March, with fresh record highs in China and internationally. “The SHAUPM in RMB saw its strongest month for a year while the March return of the LBMA Gold Price PM in USD reached its highest since July 2020,” he said. “Geopolitical tensions and Trump's unpredictable trade policies increased gold's appeal as a safe-haven asset. A weaker dollar and higher gold ETF investments pushed up prices further.”

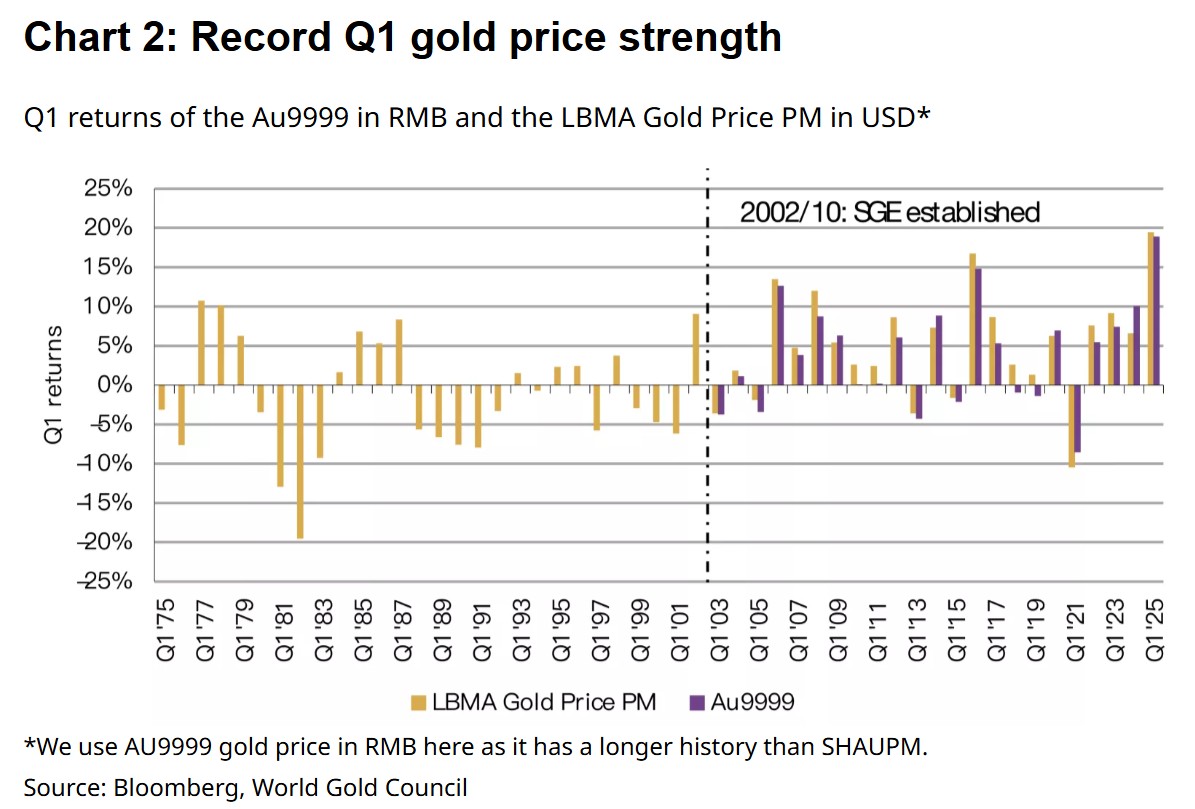

Gold’s standout performance in March also contributed to a strong Q1 with gold prices in both RMB and USD gaining 19%. “The RMB gold price recorded its strongest Q1 since 2002 – when the SGE was established – and the USD price posted its best Q1 return since 1975,” Jia wrote.

The key drivers during the first quarter included rising safe-haven demand amid global geopolitical and trade policy risks, USD weakness on concerns around U.S. growth and the Fed’s rate path, and strong inflows into global gold ETFs.

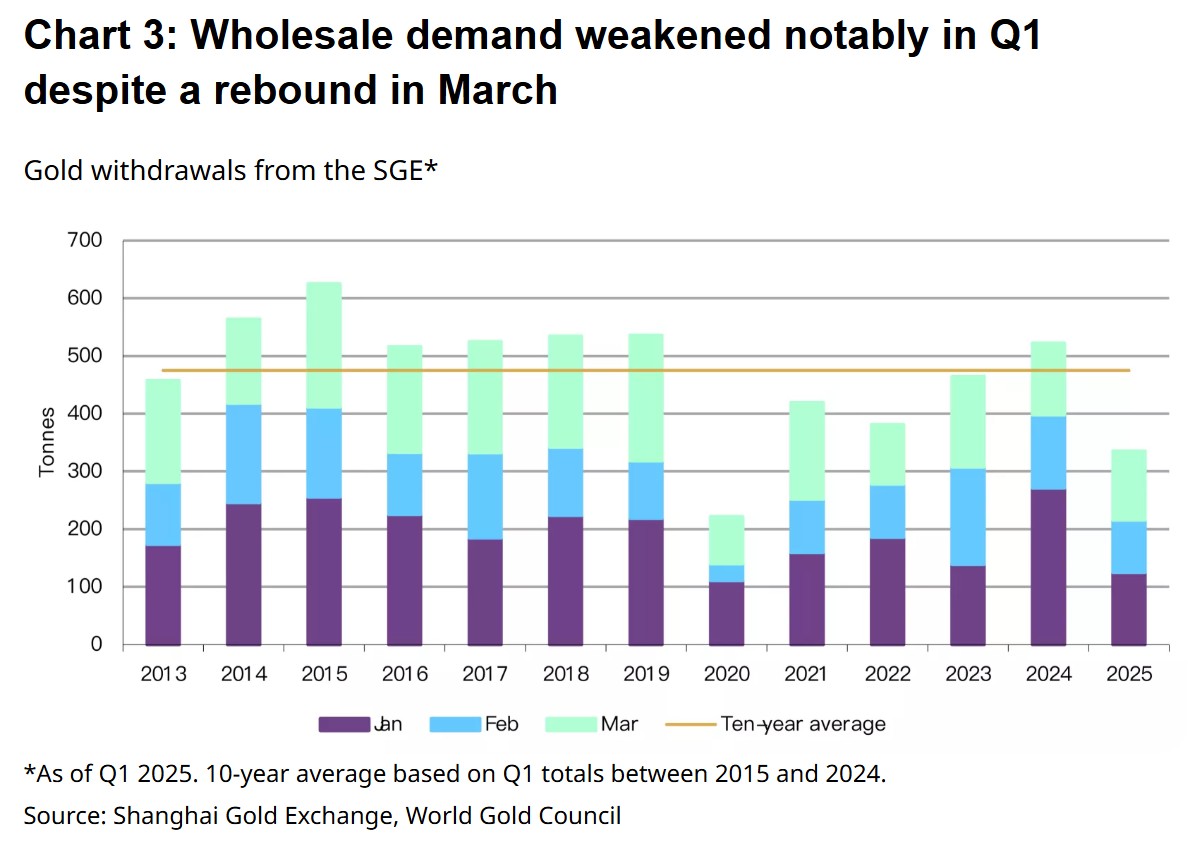

Wholesale demand weakened in Q1, however, despite a rebound in March. “Gold withdrawals from the SGE totalled 120t in March, up 30t m/m but slightly lower y/y,” Jia said. “The m/m rebound came as jewellers and banks restocked after the Chinese New Year holiday slowdown – a seasonal pattern. Continued strength in investment demand for gold may also have provided a boost. We believe a pickup in wholesale gold demand resulted in the improving local gold price premium in March (US$4.3/oz on average vs a US$1.5/oz discount in February).”

He noted that Chinese wholesale gold demand came in at 336 tonnes in Q1, which was 29% below the ten-year average and a 36% decline compared to Q1 2024.

Jia said the previous quarter’s weakness can be mainly attributed to a high base, as January 2024 saw the strongest wholesale demand on record, and the surging gold price pressured jewelry demand.

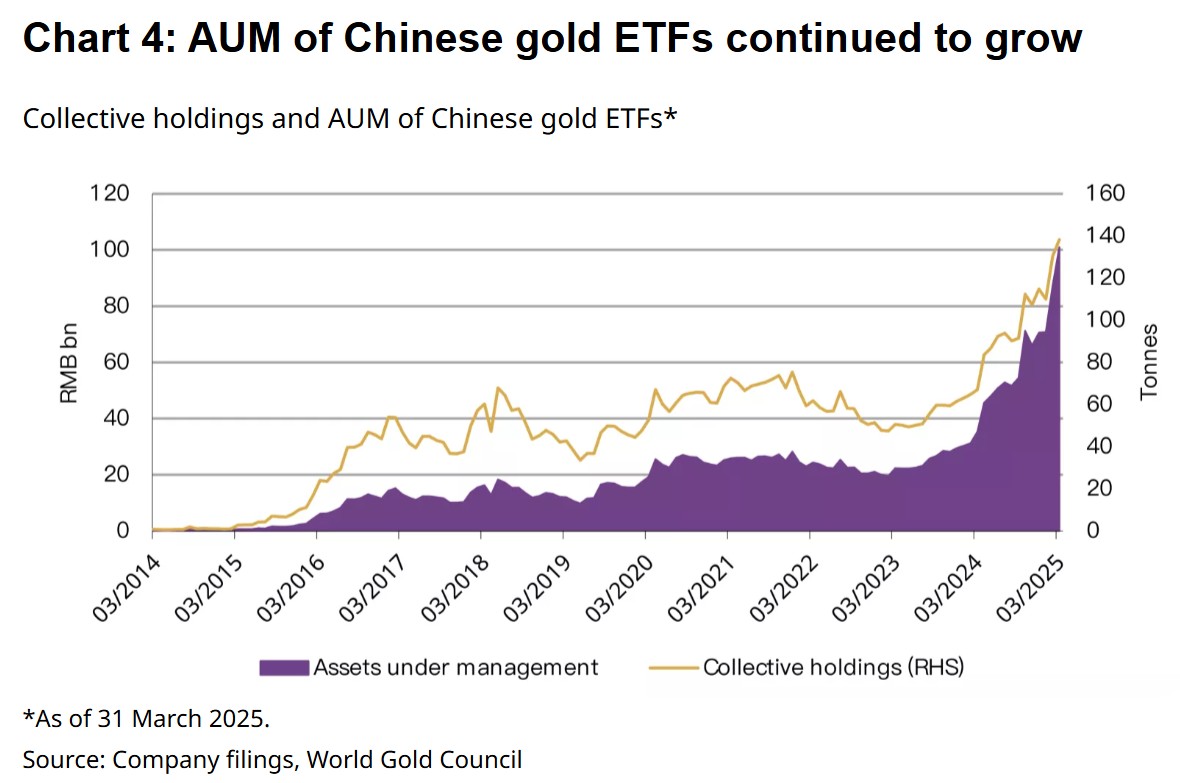

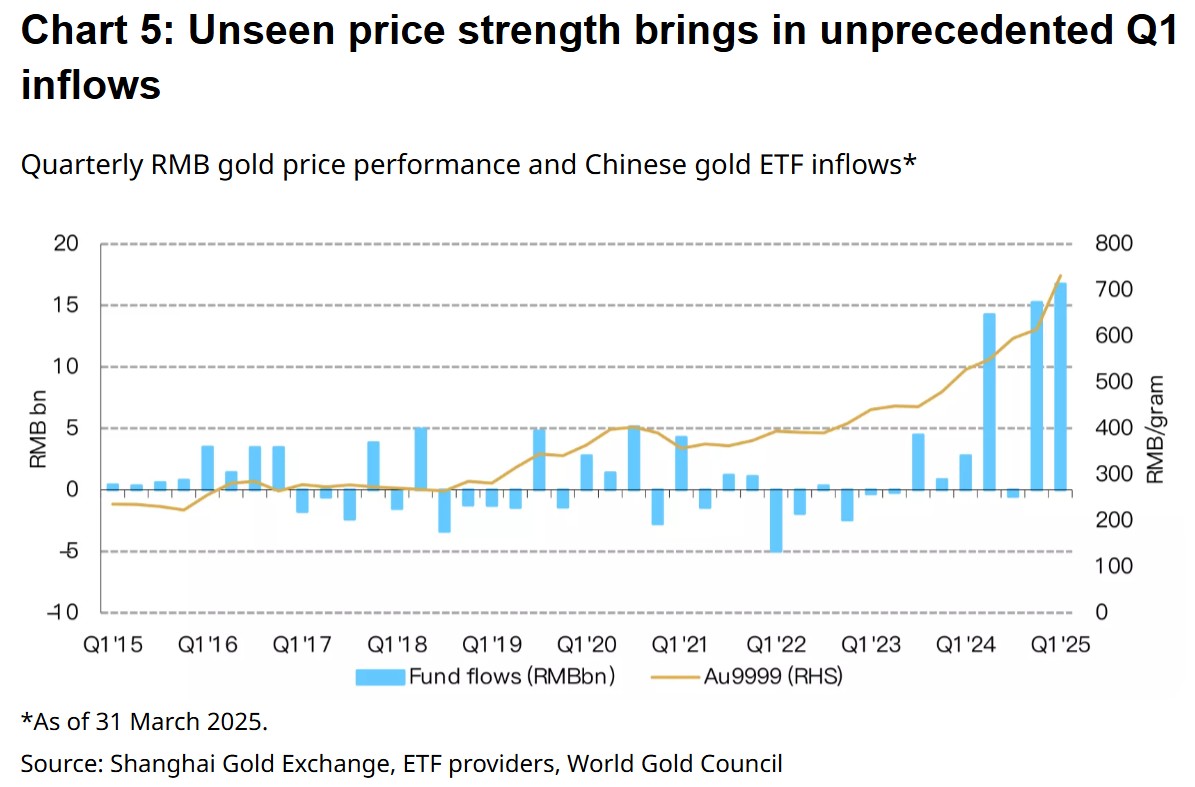

Sky-high prices did help to boost investment demand, however. “Inflows into Chinese gold ETFs sustained for a second month, totalling RMB5.6bn (US$772mn) in March,” he said. “Continued inflows and the surging gold price pushed the total AUM to another month-end peak of RMB101bn (US$14bn). Collective holdings rose further by 7.7t to 138t, also a record high.”

“The soaring gold price remained a key driver for healthy Chinese gold ETF inflows during March, while global trade uncertainties and concerns around their impact on the local economy provided an additional boost,” he added.

The strong demand in February and March also contributed to a record-setting quarter for Chinese gold ETF inflows. “The first quarter of 2025 saw inflows of RMB16.7bn (US$2.3bn), equivalent to a 23t increase in holdings – both reaching record levels,” Jia said. “The unprecedented gold price surge, shaky confidence in other domestic assets, as well as growth concerns stemming from escalating trade conflicts with the US, all contributed to strong Q1 flows.”

“And it is worth noting that record inflows continued into Q2,” he added. “During the first two weeks of April, Chinese gold ETFs’ collective holdings surged another 29t whilst total AUM rocketed 25% on sustained gold price strength and escalating trade tensions with the US.”

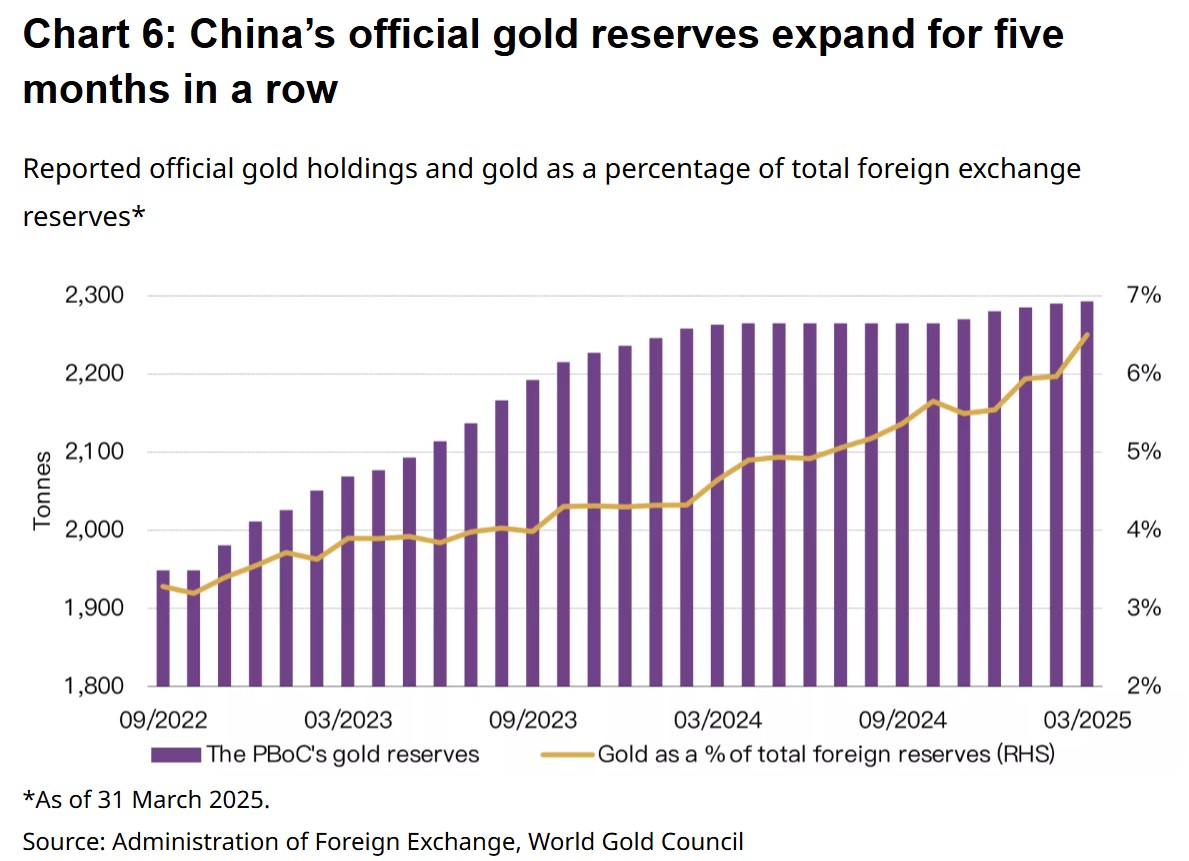

China’s sovereign gold reserves also rose once again in March. “The PBoC has announced gold purchases in each of the past five months, and in March, added a further 2.8t,” Jia wrote. “This pushes China’s official gold holdings to 2,292t, or 6.5% of total reserves. During Q1 2025 China reported purchases of 12.8t of gold.”

China’s total reserves rose by 2.3% to US$3.5tn in Q1, he said, supported mainly by a weaker dollar (which pushed up USD denominated asset prices), falling Treasury yields (which lifted bond values), and increased gold holdings combined with a rallying gold price, which surged 20% to $230 billion and added “over 1% to the quarterly increase in total reserves.”

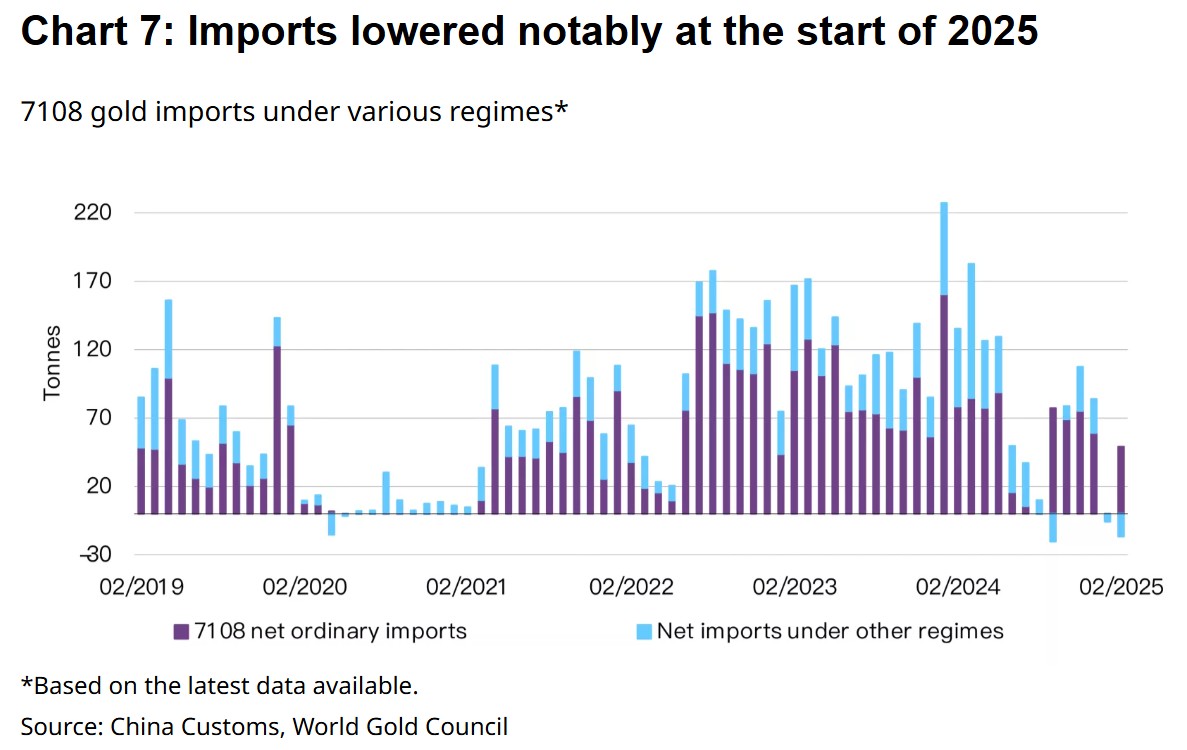

The high prices had the opposite effect on imports, however, which remained weak at the start of 2025

“Gold imports into China virtually came to a halt in January, amounting to just 17t, the lowest monthly value since February 2021 – at which time imports were hampered by COVID restrictions,” Jia said. “February imports picked up, rising to 76t. Nonetheless, they remained well below the 2024 monthly average of 102t.”

And the weakness is even more stark on a net basis. “Net ordinary imports fell to zero in January, the lowest since early 2021; they rebounded to 49t in February, yet still represented a 38% y/y plunge,” he said. “We believe fewer working days due to the Chinese New Year’s holiday, weak domestic gold demand and local gold price discounts during most of the period – which discouraged importers – were the main drivers.”

Looking ahead, Jia said the WGC expects gold investment demand will stay strong in the near term as the escalating trade war between the U.S. and China hurts growth and local assets.

“The global gold price strength, boosted by a re-structuring of the world trade order and world market volatility, will provide further support,” he said.

Chinese insurers have also recently entered the gold market, with four companies becoming SGE members in March. “Their participation should sustain long-term investment demand for gold in China, especially amid ongoing economic and trade uncertainties,” Jia said, but also cautioned that even with the upcoming May Labor Day holiday, “record high gold prices and economic worries are clouding the jewellery demand outlook.”

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-