The Battle for Indias $45 Billion Gold Industry Has Begun

(August 29, 2017 - by Swansy Afonso and Ameya Karve, Bloomberg)

India’s past and future are colliding in Anand Ghugre’s family jewelry shop in Mumbai.

“We still operate the way my father did for 50 years,” said Ghugre, 52, explaining that transactions were typically in cash and were not always recorded. “For small jewelers and the unorganized sector, most of our sales happen through personal connections. Sometimes they don’t want bills, but the jewelers can’t say no to them.”

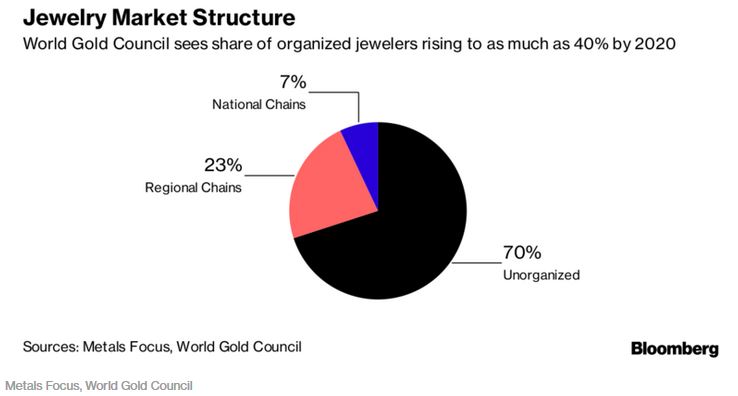

That way of doing business is under threat as the world’s second-largest gold market faces Prime Minister Narendra Modi’s campaign to bring India’s informal economy to book. About three quarters of the estimated $45 billion of the precious metal that is traded in the country each year makes its way through thousands of family-run jewelry shops that have catered for centuries to the nation’s love of gold.

Modi’s financial reforms, including demonetization and a new goods and services tax, combined with a younger generation that shops online, may usher in a wave of takeovers and mergers by big state-wide and national chains as small shops are swallowed up or close.

“The one story that we hear is that the business is becoming problematic for smaller jewelers,” said Chirag Sheth, an analyst at London-based precious metals consultancy Metals Focus Ltd. “The bigger jewelers have deeper pockets, they have larger shops, better designs and better margins. It is very difficult for a smaller guy to compete.”

Modi in November banned higher denomination notes to bring unaccounted cash back into the system and introduced tougher proof of identity for purchases, capped the amount of cash used in transactions and topped it off with the uniform goods and services tax last month.

An overhaul of the fragmented industry is also on the cards with the government said to be planning a new policy on gold that will bolster confidence among consumers, where the gifting of gold at weddings and festivals or its purchase as a store of value are deeply held traditions. Fixing quality standards and allowing supply chains to be easily tracked are ways to enhance trust.

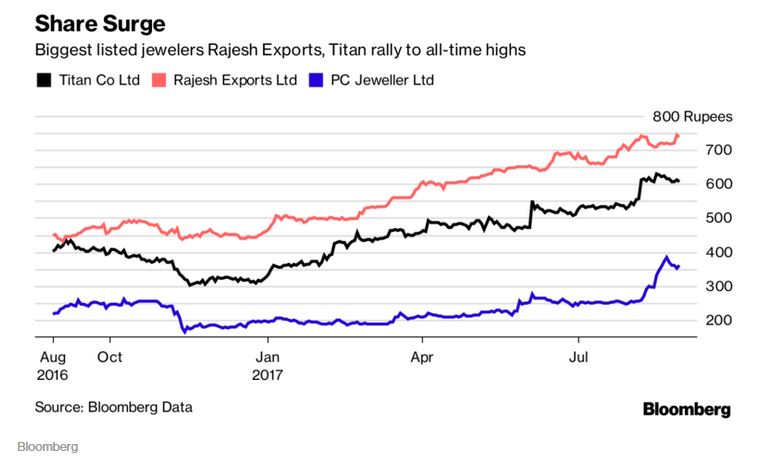

The government fixed GST on gold at 3 percent, replacing more than a dozen domestic levies. That will make it easier to track the flow of gold and harder to evade taxes, benefiting larger players like Tata Group’s Titan Co., Credit Suisse Group AG said in June.

The nation imports almost all the gold it consumes and demand last year was about 666 metric tons, according to the World Gold Council. That’s more than the entire gold reserve of the European Central Bank.

In 2015, national chains including Tanishq, owned by Titan, and regional players accounted for about 30 percent of the market. That could rise to as much as 40 percent within four years, the World Gold Council said in a report in January. And assuming GST is implemented uniformly, the shift may happen even faster, said P.R. Somasundaram, the council’s managing director for India.

The new tax will increase paperwork and costs for smaller jewelers as they try to conform, said Sheth. Jewelers will now have to file as many as 37 returns, he said.

For the big players, the reorganization of the industry will improve their credit profile, according to ICRA Ltd., the local unit of Moody’s Investors Service, which predicts a round of consolidation, where “organised players may acquire smaller entities or enter into franchise agreements.”

Over the medium term, revenues of those retailers would grow at 5 percent to 6 percent, almost double the overall industry rate, according to a June report from Crisil Ltd., the Indian subsidiary of S&P Global Inc.

Titan is seeking to add 25-30 stores every year through franchises, especially in the smaller towns in north, west and east India, said Sandeep Kulhalli, senior vice president for retail and marketing at the Bengaluru-based jeweler, on Aug. 12.

Lack of transparency in the sector made it difficult for domestic banks to lend to jewelers looking to develop workshops and hire more workers, the WGC said. But the current optimism over the industry has seen overseas investors pumping in money to bigger jewelers.

In April, Warburg Pincus LLC raised its investment in Kerala-based Kalyan Jewellers Ltd. to 17 billion rupees. Kalyan and fellow south Indian retailer Malabar Gold & Diamonds plan initial public offerings within the next two years.

For many smaller players, this is the time to expand or die, said Saurabh Gadgil, the sixth generation of one of India’s oldest jewelry outlets, which owns about 20 stores across three states.

“The next few years will be very good for the industry as the current ecosystem will bring more jewelers into the formal economy,” said Gadgil, 40, who holds a masters in business administration and he took the reins at P.N. Gadgil Jewellers Pvt. in 1999.

“We formed a SWAT team and started developing our employee- and customer-related business and professional platforms,” he said in an interview in Mumbai. “A professional organization also needs returns on investments. Just a mere happiness quotient of the customers and staff isn’t enough.”

He’s seeking funds from private investors to expand the company that was started by his ancestor Purshottam Narayan Gadgil in 1832 in Sangli, a town so small then that it’s name means “six lanes.”

For those who survive the upheaval, the potential rewards are large. India is the world’s second-biggest buyer of the precious metal and consumption is recovering after slumping to a seven-year low in 2016. Demand is projected to reach between 850 tons and 950 tons by 2020, buoyed by purchases for weddings and festivals and a growing economy, the WGC estimates.

Ghugre in Mumbai is doing what he can to adapt to the new market.

“I have told my son to do a course in digital marketing,” he said. “We need to change our strategy to compete with the bigger chains and attract the younger generation.”

Four years ago, Ghugre installed his first computers at the store, which are now being used to help file GST returns online and to develop a Facebook page for the business. But he says progress has been slow and his main hope is to win over the next generation of his aging clientele.

“A couple of weeks ago, there were heavy rains in my area, and the internet was down for eight days,” he said. “We small players will ultimately have to adapt, but it will take time.”

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-