The Stage is Set For Higher Silver Prices

(September 6th, 2021 - Baker Steel Managers)

Silver is uniquely placed as a “future facing” precious metal

The precious metals sector has faced a range of headwinds in recent months, from the prospect of higher nominal US rates, to shifting investor sentiment as the global economic recovery progresses and stock markets hit record highs. These short-term factors have put pressure on precious metals and miners but belie the strong macroeconomic undercurrents which point to higher gold and silver prices ahead. The recently released Q2 2021 results show precious metals miners’ encouraging performance has continued, with the trends of margin expansion and increasing shareholder returns indicating a positive outlook for silver equities.

Gold often dominates analysis regarding the outlook for precious metals, however as sector specialists we consider that silver and silver miners present a particularly compelling opportunity at present. We have written frequently in recent months about the two key themes Baker Steel sees for the natural resources sector: the rapidly progressing green revolution and development of green technology, and the debasement of currency through rising inflation and financial repression.

Silver is central to both themes. Precious metals are the ultimate hard asset, offering protection from inflation, yet silver also has strong green credentials, which are yet to feed into prices, due to its growing use in the clean energy revolution. With the recent sell-off having sent silver prices and silver miners’ valuations to an 8 month low, we believe the silver sector is poised for a period of recovery in the coming months, as well as offering leverage to the longer-term upcycle in precious metals and the rapid growth of green industries.

The past 12 months have been a frustrating period to be a silver investor, with silver prices having fallen by around 16% since the summer highs of 2020 and with silver miners under pressure. Baker Steel has maintained a sizable silver weighting during this period and, while this has dragged from time to time on the relative performance of our strategies, we maintain our conviction for two core reasons:

- Silver producers are among the most undervalued companies within the mining sector, on a fundamental and relative basis, with sizeable upside potential during periods of recovery for the sector.

- Silver miners offer attractively valued exposure to both the recovery of the precious metals sector and the rapid growth of green industries and the growing shortage of critical materials.

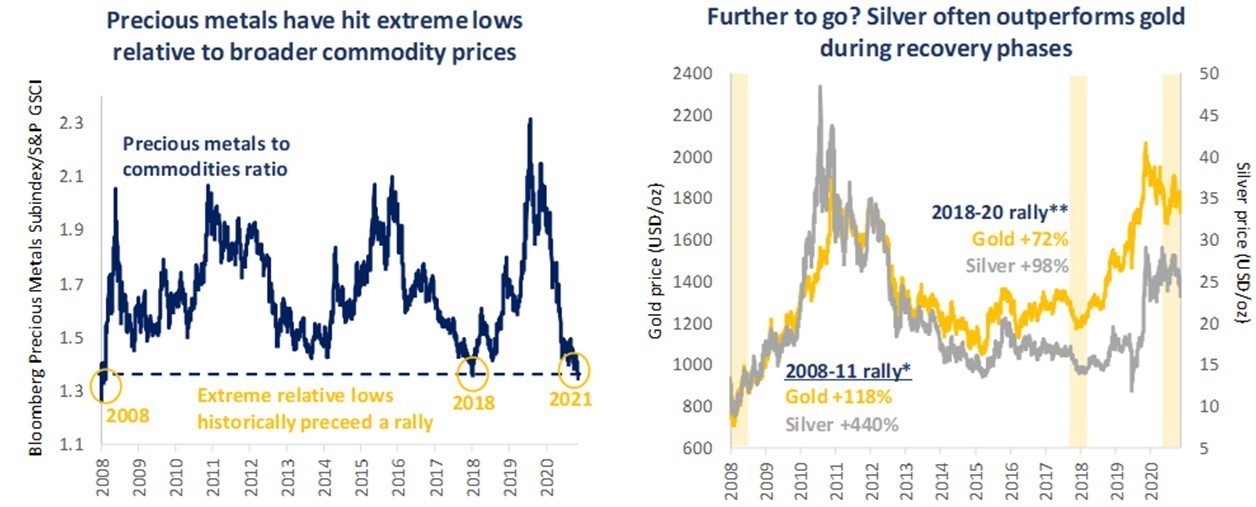

Is a recovery for the silver sector near?

From a technical perspective we see signs that we are around the bottom of this mid-cycle pullback for silver, as well as for gold. Silver’s recent lows have held above significant technical support lines at c $23/oz and in recent weeks silver prices show signs of recovery. Silver is more volatile than gold typically, and so pullbacks can be painful for investors, however the upside potential can be substantially higher. US retail demand for silver has historically been an influential factor for silver prices, however this source of demand has yet to emerge as a driving force for the current cycle. That said, the silver price’s sharp upwards move during the attempted “short squeeze” by retail speculators in January and February of this year highlighted that the metal’s price can move quickly under the right conditions.

Of course, while the technical positioning of silver may indicate a short- to medium-term opportunity for the sector’s recovery, it is the longer-term picture for silver which is arguably most compelling, perhaps more so than for any other metal, given its industrial applications relating to rapidly growing green technologies, most notably, the production of solar voltaic cells.

Where are we in the precious metals bull market cycle?

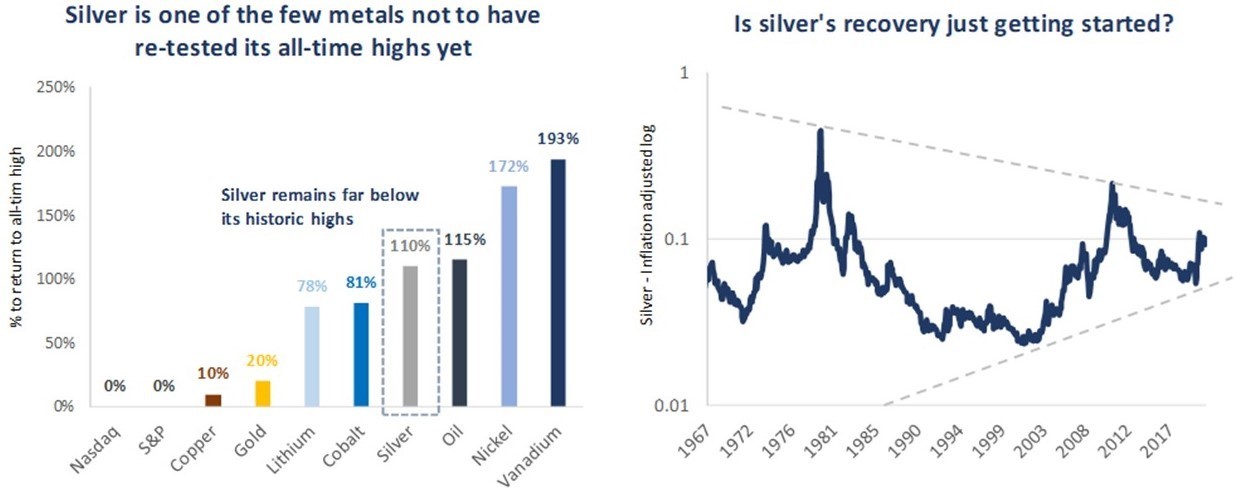

We consider that precious metals are midway through a long-term upcycle, driven primarily by expanding money supply, persistent low and negative real interest rates, rapid debt expansion and ultimately fiat currency debasement. The gold price made new highs in 2020, boosted by concerns over the economic impact of the COVID-19 pandemic, while silver has made encouraging gains since its lows in the middle of the last decade. Despite the sector’s progress in recent years, we believe silver’s recovery may be just getting started. Historically when gold makes new highs, so does silver, and so the very fact that silver has not yet retested its all-time highs in this cycle is in itself an indication that there is much more to come from the metal.

We believe the core drivers of the precious metals bull cycle, mentioned above, not only remain in place but have been exacerbated by policy response to the COVID-19 crisis. The pace of debt expansion has accelerated, while vast stimulus packages have been implemented with strong public support. US stimulus spending since the start of the COVID-19 crisis has reached $6.7 trillion, including the recently passed $1.2 trillion infrastructure bill, an enormous sum by any standard. With a further $3.5 trillion “human infrastructure” bill being proposed by the Democrats, we anticipate this vast sum will continue to expand.

These policies appear to be achieving their goals, boosting economic recovery and protecting employment, however a direct consequence of these measures has been a rapid increase in money supply, with US M2 increasing by 24.8% during 2020 and 11.3% year-on-year at the end of July 2021. A further much-publicised consequence is the rising inflationary pressure as economies have reopened in recent months. The prospect of a period of heightened inflation presents a potent catalyst for precious metals, which have historically proven to be effective inflation hedges. Whether inflation will slow as the recovery progresses, as many policymakers predict, or remain persistently high, remains to be seen. Inflation and expanding money supply are key factors for the precious metals sector.

In light of the economic recovery and signs of rising inflation, speculation over potentially higher US rates has resurged, dragging on the performance of precious metals in recent months. Higher US nominal rates appear likely, but it is our view that the limitations on central bankers’ scope to raise rates will become increasingly clear as rate hikes approach. Strong economic data from the US and other major economies have boosted the hawkish case for higher rates, yet with a nascent recovery built on heavily indebted businesses, consumers and administrations, the risks of tightening monetary policy appear substantial.

We consider the medium- to long-term outlook for silver and gold to be highly positive, although it is likely that in the short-term, we may continue to see volatility and mixed sentiment persist for the sector as investors look to the Fed for an indication of future monetary policy direction. Overall, we are convinced that such a long period of unprecedented loose monetary policy and heavy-handed stimulus spending are likely to have lasting consequences for consumer prices, debt levels and monetary policy direction. Monetary debasement will continue, strongly favouring hard assets such as precious metals, and given the leverage which silver and silver miners offer to higher precious metals prices, we anticipate a sizeable upwards move in the sector as the impact of policies of financial repression become apparent.

The green “industrial revolution” will transform silver demand

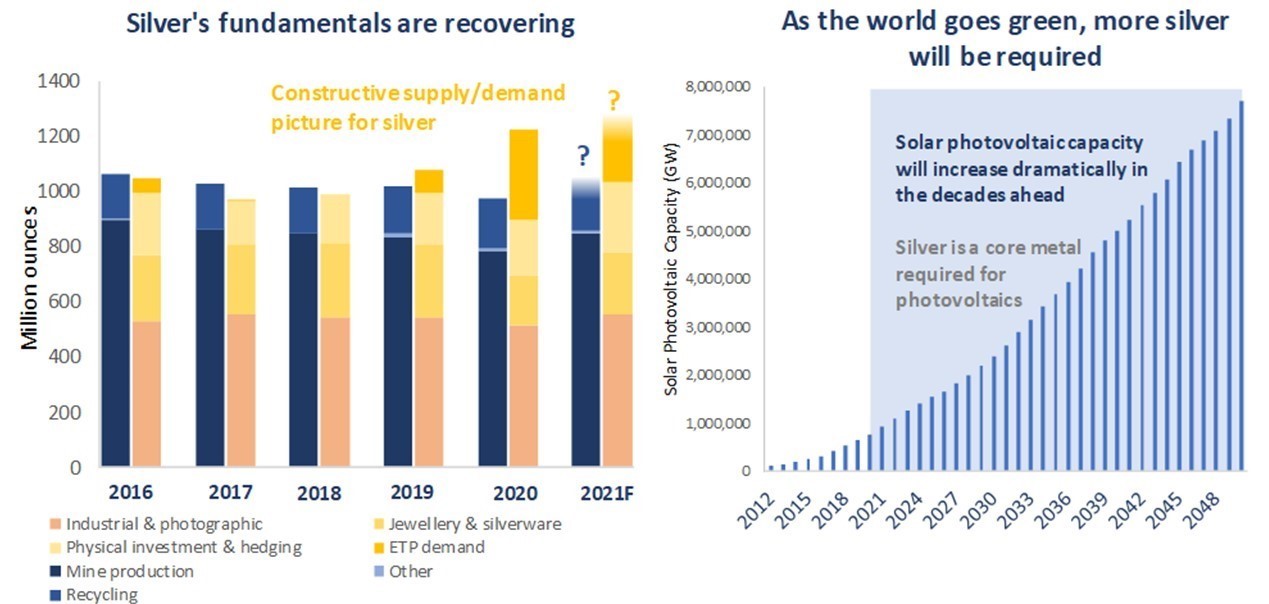

Physical demand for silver is quite different from gold, being simultaneously an investment through bars and coins, a luxury good used for jewellery and silverware, while also being an industrial metal with applications across industries.

Historically photography was a key source of demand for physical silver, accounting for around 35% of total demand in 1999 (USGS), before collapsing by around -70% to today’s demand levels. In 2021 about half of silver demand is from industrial activity. Solar photovoltaic (“PV”) capacity is expanding rapidly as the technology becomes more affordable, energy demand increases, governments offer support, and environmental awareness among consumers grows. It is anticipated that demand from solar PV could equal or exceed the silver volumes previously used in the photographic film industry. Projections for solar photovoltaic development indicate a rise of +180% in ten years, +459% in 20 years and +720% by 2050. Even with some inevitable substitution of silver for more cost-effective materials, increases of this magnitude promise to transform the silver industry.

With the advance of new technologies, we expect silver demand to grow as the metal’s usage rises across a number of other green industries. Notably, silver demand from the auto industry appears set to increase significantly in the coming years as the rollout of electric vehicles (“EVs”) gains pace. The auto sector currently uses over 55moz of silver annually, with demand forecast to rise to almost 70moz by 2030. Silver’s conductivity and resistance to corrosion make it a critical component for electronics, and accordingly average silver loadings for EVs are estimated to be around 74% higher than for internal combustion engine powered light vehicles. EVs are expected to account for almost half of silver demand from the auto industry by 2040, making this industry a key element of future silver demand (Silver Institute).

Silver miners offer leverage to the upcycle in precious metals as well as the “green revolution”

Silver and silver miners have undergone a period of consolidation in recent months, as has gold, in line with previous mid-cycle pullbacks. For investors seeking exposure to the two key themes facing the natural resources sectors, the upcycle in precious metals and the growth of the green revolution, we consider that silver and silver miners have a central place in a diversified portfolio. It is our view that these themes will underpin the next leg up for silver prices in the months ahead, alongside gold, while also driving a secular bull market for a range of speciality metals associated with green industries. Silver miners are of particular interest for us, as long-term investors in this sector, as there is a scarcity of quality silver producers available to investors. High quality, well-managed silver producers have historically traded at premiums in times of high silver prices and strong investor interest in the sector.

Recent weeks have highlighted the volatility which can face the precious metals sector as investors mull the prospects for higher rates, however in our view nothing has changed with regard to the bullish outlook for precious metals. Persistent low real rates, vast stimulus, debt expansion, along with a rapid expansion of money supply, indicate monetary debasement will continue, strongly favouring hard assets such as precious metals. Importantly, the precious metals sector has not yet reacted to the implications of persistent higher inflation, but as evidence of further inflationary pressure grows, we expect this to benefit silver and gold, as it has done historically.

With this in mind, we would consider dips such as those we have seen this week to be an opportunity for investors to build a position in the sector, both for diversification purposes and for exposure to the recovery of this oversold sector. Baker Steel’s strategies are positioned for this opportunity through our investments in high quality silver producers. As with our exposure to gold equities, we are focused on those silver producers with the highest quality assets, strong margins and effective management teams, which operate in an ethical and sustainable manner in line with our own ESG principles, with the objective of delivering superior risk-adjusted returns relative to a passive investment in the sector.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-