Why commodity prices could stay higher for longer

(October 27, 2017 - by Goldman Sachs)

Commodity prices stormed higher in the decade to 2012, fueled by a mismatch between Chinese demand and global supply, creating supply shortages that led to substantial gains in many commodity markets.

China wanted everything and more, and miners weren’t in a position to deliver it.

However, that all changed in 2012.

Chinese demand slowed and supply, encouraged by previous strength in prices, arrived in abundance, seeing many markets move from being in deficit to surplus, creating downside pressure in many markets, acute in some instances.

Now, after a roller coaster rise over the past decade or so, commodity prices, as a whole are starting to recover, thanks in part to a lessening supply as high-cost producers shutter operations.

As Goldman Sachs’ Metals and Mining equity research team, comprising of Craig Sainsbury, Eugene King and Humberto Meireles note, part of that supply reduction has come from mine closures in China.

They explain:

One of the unforeseen consequences of the China commodities boom was the uplift in domestic Chinese production of metals. Insatiable metals demand in China also saw China’s contribution to global supply increase from circa 10% in 2002 to circa 20% today. Much of that increase in supply was from low-grade, high-cost operations with a negative environmental footprint. With China now increasing supply-side structural reform, domestic volumes are being negatively impacted. Consequently, Chinese production volumes of many materials are likely to be lower in 2017 than in previous years.

With China cutting capacity, Sainsbury, King and Meireles say that production volumes from abroad need to remain firm in order to maintain a balanced market.

However, as they point out, many mining firms have not been investing in exploration and mine development recently, relying instead on existing assets and firmer commodity prices to help lift capital returns to investors.

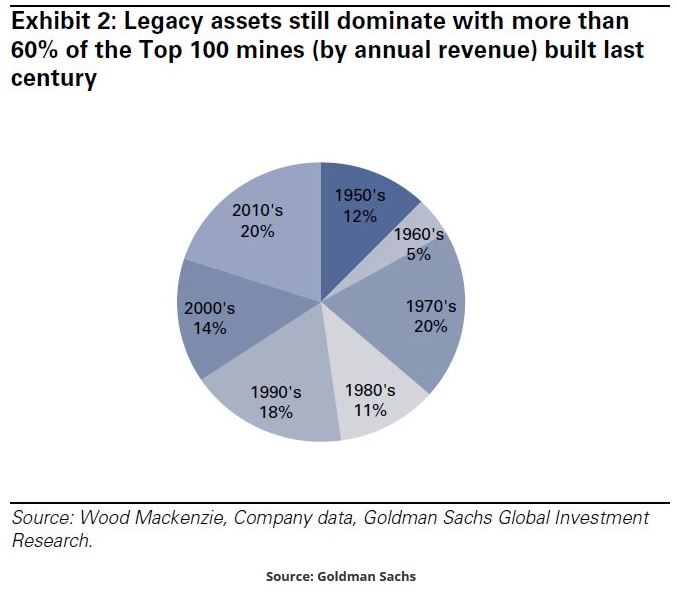

Whilst miners are making more money in the current commodity price environment, they appear more focused on returning capital than investing in regenerating supply. Of every dollar of excess cash generated by strong prices, we estimate 53 cents is being returned to shareholders. This is returning sector exploration and mine development to levels last seen a decade ago. New global mine development has slowed. Of the Top 100 mining assets globally, over 60% were commissioned last century.

Here’s an interesting chart from Goldman showing when today’s major mines by annual revenue were built.

Many of these major assets are clearly ageing.

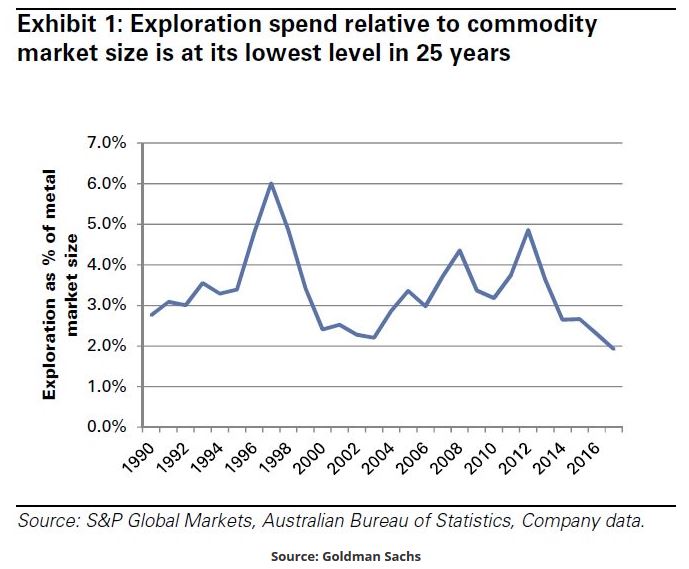

And, as this equally interesting chart shows, exploration expenditure as a percentage of the total metals market has now fallen to levels not seen in at least a quarter of a century.

The combination of supply cut in China, ageing mining assets and a lack of new investment has got Sainsbury, King and Meireles excited about what that could do for prices, suggesting it is potentially setting up a period of continued under-supply, leading to stronger commodity prices for longer.

If China continues to focus on supply-side reform, we highlight commodities such as steel and aluminum as materials where Chinese production could be down materially year-on-year. China’s export of such commodities could also decline significantly, helping improve ex-China supply/demand balance and sustain prices at higher levels. If the pricing response is similar to what we saw in 2016 for iron ore and coal, the pricing upside could be significant in 2018-20.

The Goldman Sachs’ research team says the key factor underpinning this bullish outlook will be for commodity demand to stay stable.

As the world’s largest commodity consumer, that will almost certainly be determined by China.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-