Fed’s Dovish Tilt Adds Fresh Fuel To Precious Metals

(December 18, 2023 - Ole Hansen)

Summary: Gold and silver trade sharply higher following the December FOMC meeting where surprisingly dovish comments from Federal Reserve chair Jerome Powell triggered a major drop in bond yields as traders lifted 2024 rate cut expectations from four to six 25 bps rate cuts. With this in mind our belief in even higher precious metal prices next year has only been strengthened with lower real yields and lower funding cost potentially attracting fresh demand from ETF investors who have been net sellers for the past seven quarters.

Key points in this note

- Gold and silver rally after Fed rate focus changes to cuts from hikes

- Lower real yields and lower funding cost expected to attract fresh demand through ETFs

- Santa rally or not, gold is heading for another strong annual performance

In our latest gold market update we discussed the short-term negative impact on positioning of the early December rally when short covering and ‘fear of missing out’ bids briefly drove gold above $2035 before suffering a +160-dollar reversals. We highlighted the risk the market had reached levels that was hard to align with current fundamentals, not least considering no official nod had yet been given to support the succession of rate cuts priced in by the market.

Yesterday, however, the FOMC declared victory over inflation, and while the change in their dot plot from two to three rate cuts was nothing special, the subsequent comments from Federal Reserve chair Jerome Powell were surprisingly dovish. At the press conference, Powell focused on the risk of causing unnecessary harm to the economy by leaving rates too high as inflation falls. “We’re aware of the risk that we would hang on too long,” he said. “We’re very focused on not making that mistake.”

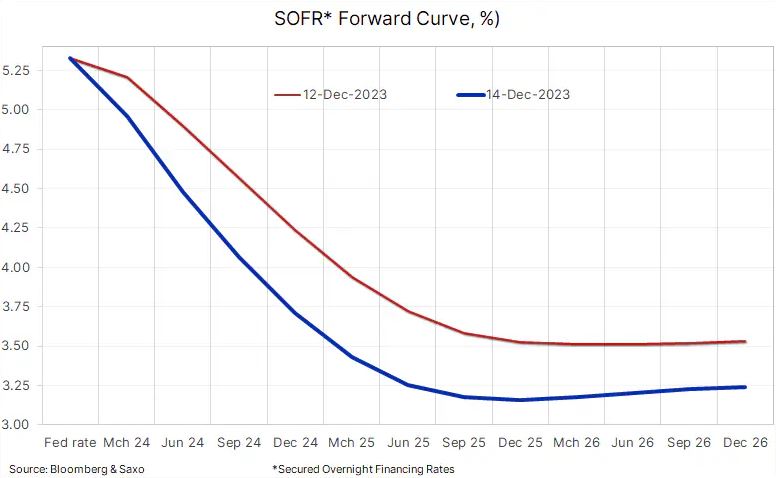

The market reaction was very decisive with bond yields slumping, not least at the short end where 2-year Treasury notes has seen a two-day decline of 43 basis points to 4.3% while the 10-year benchmark yield trades back below 4% after briefly trading above 5% less than two months ago. While the FOMC Dot plot lifted the number of rate cuts next year to three from two, the swap market went a lot further to price in six rate cuts during the next year to 3.71% with the through in rates expected by December 2026 at 3.16%, a level that given the current inflation projections and expectations for a soft landing should bring rates back to a neutral stance. If, however, the soft-landing turns into a recession, an additional four to six rate cuts may be needed in order to achieve an accommodative policy rate.

Small Santa rally ahead of a potential strong year for gold and silver

In this video update we follow up on recent articles which highlighted the fact gold and not least silver had seen strong December returns during the past six years, and wondered whether we would see a repeat this year. Following the recent deep correction, gold has returned to trade near unchanged on the month while silver remains down around 5%. Santa rally or not, gold especially is nevertheless heading for another strong annual performance, currently at 12%, and its best year since 2020 when bullion surged 25%.

In the months and quarters that followed the start of the three most recent rate cutting cycles, gold performed very well, and the market is likely to gear up for an attempted repeat in the coming months with the first rate cut now priced in to occur at the March meeting.

We maintain our long-held bullish outlook for gold into 2024, and with the FOMC finally onboard the rate cutting train, the pace of cuts next year will depend on how inflation develops and whether a soft landing can be achieved. In addition, it is also worth mentioning that central bank demand potentially is heading for another record year, with more than 1000 tons being removed from the market for a second year running, thereby providing a soft floor under the gold market. Central bank buying of gold, has according to estimates from the World Gold Council added around 10% to the price this year, and is therefore one of the main reasons the yellow metal has managed to rally despite surging real yields, and why silver suffered more during periods of corrections as they do not enjoy that constant and underlying demand.

In the coming weeks we will be watching ETF flows and look for signs of a change in behavior towards gold from investors who have been net sellers during the past seven quarters. We believe the prospect for lower real yields and lower cost of carry will be the determining factors that eventually will drive fresh demand, and together with continued central bank demand and tactical positioning from hedge funds, the prospect of reaching a fresh record high looks increasingly likely.

-

Gold & Silver Moving Above Resistance Levels By

Gold & Silver Moving Above Resistance Levels ByJuly 22 2026

-

Gold & Silver Moving Higher On Strong Demand By

Gold & Silver Moving Higher On Strong Demand ByJuly 21 2026

-

-

Gold & Silver Prices Firming Above Support – July CoinStats By

Gold & Silver Prices Firming Above Support – July CoinStats ByJuly 20 2026

-

China Gold Market Update By

China Gold Market Update ByJuly 20 2026