We believe gold has entered a new bull market. Here are four reasons why

(August 23, 2017 - by James Luke and Mark Lacey)

Despite significant US dollar weakness, gold price performance has been muted recently.

It has been held back by factors such as a rebound in real interest rates and increased stability in the Chinese yuan, which has dampened near-term investment demand for gold in China.

But these are short-term factors, which do not change our view that gold has entered into a new bull market. As we have discussed previously, there are four main reasons for our stance:

- Global interest rates need to stay negative

- Broad equity valuations are extremely high and complacency stalks financial markets

- The dollar might be entering a bear market

- Chinese demand for gold has the potential to surge (indeed, investment demand in China for bar and coin already increased over 30% in the first quarter of 2017, according to the World Gold Council)

Right now it is the second of these factors which we think is particularly pertinent.

At this time of heightened geopolitical risk, when Venezuela is on the brink of chaos and tensions are growing between North Korea and the US, there is the possibility of an event in the coming months which causes investors to seek to reduce their risk exposure.

In such circumstances, we strongly believe gold could turn out to be an underowned and well-priced insurance policy.

Why do we think there are high levels of complacency?

Complacent (definition) – “pleased, especially with oneself or one’s merits, advantages, situation….often without awareness of some potential danger or defect” (dictionary.com).

Let’s start with the US stockmarket. The S&P 500 made an all-time high of 2478 in July and is now up just under 11.5% year-to-date (source: Bloomberg, 17 August 2017).

The valuation of this index is expensive on a variety of measures. Whether we look at simple price/book, trailing price/earnings or enterprise value/cashflow (each of which are different ways to value a company), the index is trading on valuation multiples which are 60% to 100% higher than the historical median over the last 90 years.

Whichever your preferred metric, historical regression analysis suggests expected returns for equities, from today’s starting point, are very low.

The latest justification for current high valuations include President Trump’s drive to cut corporate tax and the belief that companies’ cost of capital being at an all-time low supports future earnings growth.

US companies may well receive a welcome reduction in the corporate tax rate, but the low cost of capital argument is flawed. Increasing interest rates are not supportive for equity valuations that are already high (versus history) as companies’ cost of capital increases. As unemployment continues to fall, inflation will start to pick up at the margin, regardless of the lag. Like it or not, we are firmly in a cycle of increasing nominal (not real) interest rates.

Does gold really perform well in weak equity market environments?

If we look at history for guidance, then we see gold has the potential to perform very well in periods of stockmarket weakness.

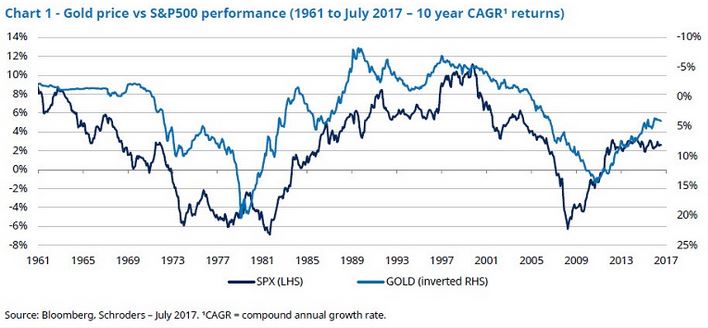

Gold’s perceived “safe haven” status is well-supported with hard evidence. For example, if we look back at gold price performance between 1961 and July 2017 (see chart 1 below), it is very clear that gold price annual returns were positive, particularly during periods of high inflation, while stockmarket returns were negative.

We see no reason why this relationship should not continue in the future; an argument for holding a minimum weighting in gold or gold equities in a well diversified portfolio. It is important to remember, however, that past performance should not be used as a guide to future performance.

Past performance is not a guide to future performance and may not be repeated. For illustrative purposes only and not to be considered a recommendation to buy or sell.

High equity valuations alone are not a reason to bang the table hard to promote the upside in gold prices, but when overall market complacency is high, the risk reward looks compelling.

It is a known fact that the best time to buy insurance is at a time when the insurers don’t think it is very likely that the “risk event” will happen. For example, in the UK, household insurance premiums to cover flood risk increased by as much as 550% post the flooding in 2007 and again in 2014.

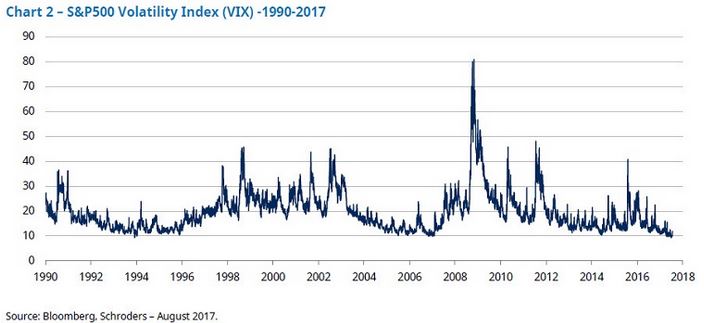

Which brings us on to the VIX, an index which illustrates the implied volatility of the S&P 500 over the next 30 days. The VIX is based on the implied volatility priced in to the exchange traded options of the equities underlying the S&P 500.

Past performance is not a guide to future performance and may not be repeated. For illustrative purposes only and not to be considered a recommendation to buy or sell.

At the moment the VIX is trading at a 27-year low. Investors are currently pricing in not just a stable pricing environment for the S&P 500 for the next few months, but basically the most benign risk environment in the history of the index.

To us, this is odd from many angles. Not least because current extreme equity valuations are set against the startling fact that global central banks are moving towards an attempt to reverse the most extreme set of policies in the history of monetary policy. More visceral external factors are also lurking in the background.

From our perspective, it is difficult to see how the market’s implied volatility does not pick up over the coming months as any external shocks will result in implied volatility increasing, given that valuations of broad equities appear overstretched. Not gold equities though; we believe they are cheap and our holdings are currently discounting gold prices of less than $1,200/oz. At the time of writing the gold price is $1291.

Please remember that past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-