Why Gold is More than an Insurance Asset

(April 18, 2018 - by Wayne Gordon)

With higher US inflation, a weaker US dollar and geopolitical tensions on the horizon, Wayne Gordon explains why he thinks gold prices will rise even higher in the long term.

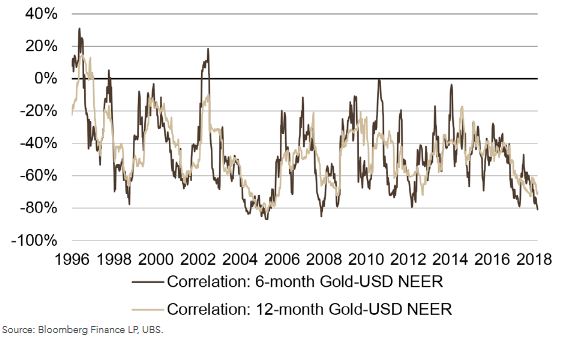

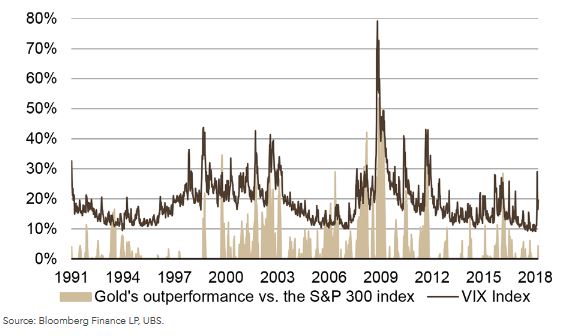

Gold’s three masters – real US interest rates, the greenback and fear itself such as (geo-) political risks – strongly drive the metal’s price direction. As gold is a non-yield-bearing asset, investors are most interested in the yellow metal’s negative correlation to real rates and the dollar and its positive correlation to fear – i.e. it tends to have a low correlation to equity markets (Figure 1). This last relationship appeared to break down in early February, with the S&P 500 declining 6%, the Chicago Board Options Exchange Volatility Index (VIX) spiking above 40 and the gold price falling by 3% (Figure 2).

Investors have begun to question gold’s claim as a hedge against stock market moves and volatility, particularly its longer-term “fear benefit” – but not us. We believe the catalysts to this surge in equity market volatility explain gold’s recent counter-intuitive behaviour, and see gold’s response to new Federal Reserve Chair Jerome Powell’s hawkish testimony as evidence that its three masters are alive and well. Also, the fact that gold fell less than equities highlights its lower volatility compared to equities.

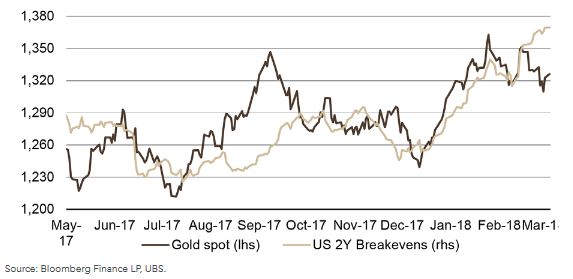

So, with the 2017 Goldilocks environment for risk assets likely over, gold’s historical correlation to financial markets should provide diversification value in a portfolio context. Likewise, as the greenback is expected to weaken again and inflation to strengthen this year, gold’s role as an inflation and currency hedge should prove to be efficacious (Figure 3).We acknowledge higher real rates towards the year-end and beyond are an inevitable headwind of varying strength, though gold’s link to real rates has weakened since December.

Funding costs reappraised, not fundamentals

The most recent shakedown in markets did not feature the usual threads of past “risk-off” events like the 2013 taper tantrum, such as sharp tightening credit conditions and the emergence of growth-cutting capital and current account imbalances. The recent sell-off was caused by a faster increase in US wages, which triggered inflation and interest rates concerns, and not by a fundamental reappraisal of earnings or growth expectations. This is the crucial point, as gold’s reaction to brief corrections are more muted than those during systemic risk-off events.

We have found that gold typically thrives amid deeper, longer-lasting and fundamentally driven bear markets, which are usually associated with a deteriorating macroeconomic outlook. Alternatively, gold’s performance is usually tepid when equities rise. A good analogy is home insurance: homeowners pay an insurance premium each year hoping the house doesn’t burn down, but if it does you redeem the policy. Here, we see gold’s “insurance characteristics” as becoming increasingly relevant for investors.

But even if the insurance is not needed, gold could still offer value. If the US dollar slides (which we expect), emerging economies become wealthier while mining costs increase. Prices could therefore advance irrespective of US inflation, making gold more than just an insurance asset.

Gold’s investment case

We see the gold price falling in the short term and rising in the long term. Here’s why:

Short term: Fed funds adjustment vs. trade worries

Jerome Powell’s testimony raised expectations of the federal funds rate rising more quickly this year and next – we see four this year and three next. Hence, the curve flattened towards the end of February, after it steepened in January – a bearish development for gold. Net-long speculator positioning was the other red flag in such an environment. As such, we expected gold to come under pressure, which it did by the end of February. By early March, gold bounced after US President Donald Trump announced additional import tariffs on aluminium and steel products.

We don’t think the tariffs will hurt trade globally and don’t believe it will spark an all-out trade war. But they do damage confidence and retaliation by one or more of its trading partners, particularly China, cannot be ruled out. Therefore, while unexpected trade and geopolitical sparks could bolster gold, our base case is for prices to weaken ahead of the Fed meeting on March 20–21.

Long-term: Inflation, a weak US dollar and choppoer markets

Our base case calls for prices to again trade higher in 12 months, supported by:

- Broad US dollar weakness: Gold’s negative correlation to shifts in the US dollar has strengthened this year – we forecast the EUR/USD exchange rate at 1.28, GBP/USD at 1.45 and USD/JPY at 100 in six months.

- Higher inflation and moderate Fed rate hikes this year: We expect US inflation to rise further this year as labour markets tighten and the Fed to hike once each quarter. Gold has historically performed strongly during such periods, as long as real US rates remain low to moderate or fall.

- Less stable equity and bond markets: While we believe equity markets should recover, we are entering choppier waters in which fears of higher inflation and interest rates could start to compete with, or even overwhelm, hopes for higher growth. This speaks to gold’s usual positive correlation with market uncertainty.

Correspondingly, we think gold prices may rise even higher. Higher US inflation and a weaker US dollar look unavoidable, while geopolitical tensions, particularly as US midterm elections approach, could give further upside to the yellow metal. The bearish price risk to gold remains a more aggressive Fed, which would see a sharp rise in real interest rates. This could hurt gold at first, though the subsequent impact on markets and growth expectations would likely support gold at a later stage.

The main driver of the yellow metal currently is the US dollar.

Figure 2: Gold adds value as an insurance asset.

Gold outperforms equities when volatility soars (VIX Index).

Figure 3: Higher inflation expectations are supporting gold prices .

US 2-year breakevens in %.

-

Gold And Silver Continue To Build Excellent Support By

Gold And Silver Continue To Build Excellent Support ByJuly 31 2026

-

The Day Gold And Silver Turned Bullish For 2026 By

The Day Gold And Silver Turned Bullish For 2026 ByJuly 30 2026

-

China’s Gold Imports Jump 89% In First Half As Prices Retreat By

China’s Gold Imports Jump 89% In First Half As Prices Retreat ByJuly 30 2026

-

-